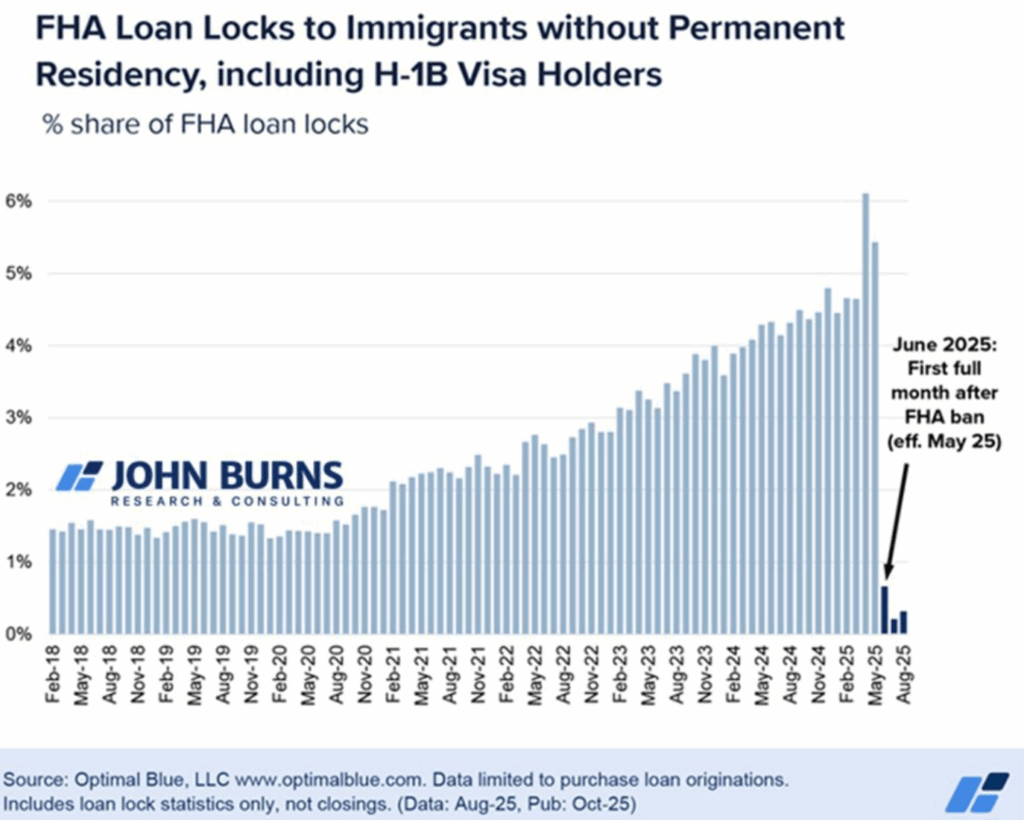

6 doesn’t sound like a lot. But an additional 6 percent demand for houses drives up costs more than 6%.

6% is a lot.

Adding 5% more cars to a city can make traffic 25% worse.

Same situation. 6% can take a buyer’s market and make it a sellers one.

It’s a big deal.

The Federal Housing Administration today announced that non-permanent residents are no longer allowed to access FHA-insured mortgages, part of a broader effort by the Trump administration to tighten immigration policies.

An example of a non-permanent resident includes an individual with a work visa. Non-permanent residents were previously eligible for FHA-insured mortgages provided the property will be the borrower’s principal residence, the person has a valid Social Security number and is eligible to work in the U.S., according to the agency’s website.

In a mortgagee letter and a Title I letter, the FHA removed the nonpermanent resident sections in its residency requirements for mortgages. The letters clarify that going forward, mortgagees must determine residency status of the borrower based on information provided on the mortgage application and other applicable documentation.

h/t Effective_Reach_9289