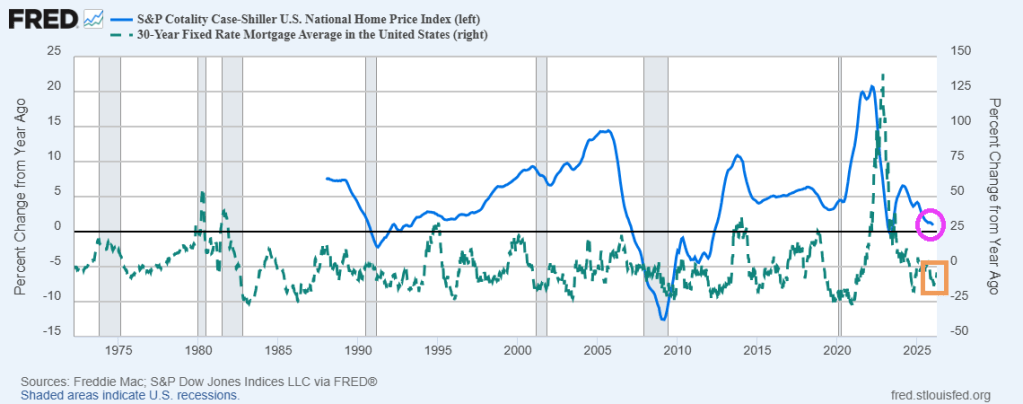

Mortgage rates moved even higher again last week, as the war with Iran continues to stoke fears of inflation. As a result, total mortgage application volume fell again, down 10.4% from the previous week, according to the Mortgage Bankers Association’s seasonally adjusted index.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances, $832,750 or less, increased to 6.57% from 6.43%, with points remaining unchanged at 0.65, including the origination fee, for loans with a 20% down payment.

Applications to refinance a home loan, which are most sensitive to weekly interest rate moves, dropped 17% for the week and were 33% higher than the same week one year ago. Earlier this year, when rates were lower, refinance demand was more than twice what it was the year before.

“The 30-year mortgage rate, now at 6.57%, reached its highest level since last August and is up half a percentage point from just one month ago,” said Mike Fratantoni, MBA’s chief economist, in a release. “Refinance application volumes declined sharply again last week, and are down more than 40% compared to last month.”

https://www.cnbc.com/2026/04/01/weekly-mortgage-refinance-demand-down.html

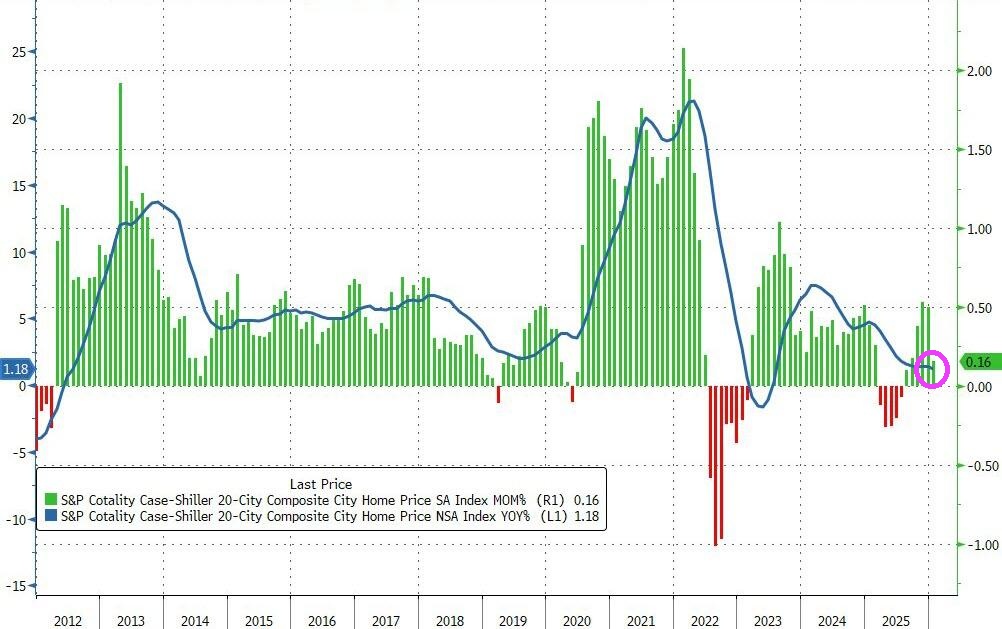

Home Prices Rise 0.9% YoY Despite Lower Mortgage Rates (Blue City Mean Reversion, New York 4.9% YoY Gain, Chicago 4.6% YoY, Cleveland 3.6% YoY While Tampa -2.5%)

We are seeing mean reversion in home prices in red cities and blue cities.

The price of homes in America’s to 20 cities rose just 0.16% MoM in January (the lowest MoM rise since August and well below the 0.35% MoM expected.

Source: Bloomberg

Home prices rose 0.9% YoY as mortgage rates have fallen. Home prices are still too high.

New York leads with a 4.9% annual gain, followed by Chicago at 4.6% and Cleveland at 3.6%, while Tampa fell 2.5%…

Redfin is reporting that homebuyers are backing out of transactions at record rates in 2026. According to Redfin’s data, nearly 14% of pending sales in Feb 2026 were cancelled, which was the highest on record going back 10 years. Buyers are canceling contracts because the housing market has shifted to a buyer’s market. To see if your area is a buyer’s market, head to http://www.reventure.app/mobile and search your ZIP code.

The Barbell Economy: Why The Middle Is Vanishing https://t.co/5C2wrCzyzn

— zerohedge (@zerohedge) April 1, 2026

There’s a pattern quietly reshaping daily life, work, and society itself. Economists now call it the “barbell economy.” Value, growth, and opportunity concentrate at the two extremes—ultra-cheap utility on one end, premium experience and status on the other—while the broad, reasonable middle thins out. Once you start noticing it, you can’t unsee it. And the data show it isn’t a fleeting trend.

Start with something as ordinary as dinner. Fast-food drive-throughs, delivery apps, and value menus deliver speed and rock-bottom prices with almost no human interaction. At the opposite pole, tasting menus and farm-to-table experiences turn meals into curated stories worth premium prices. The casual sit-down restaurant is struggling or closing—that reliable neighborhood spot that was neither rock-bottom cheap nor luxurious.

The same appears in travel. Airlines sell ultra-low fares for tighter seats but tack on fees for seat selection, bags, and boarding, while business- and first-class cabins keep expanding, with more space, better food, and priority service. Premium-cabin bookings on U.S. domestic flights have grown nearly three times faster than economy seats since 2020. Hotels follow suit: luxury and upper-upscale properties posted stronger revenue growth per available room (RevPAR) in early 2025 than midscale or economy tiers, where occupancy often hovers in the mid-50 percent range and room rates struggle to keep pace with inflation.

https://www.zerohedge.com/personal-finance/barbell-economy-why-middle-vanishing