While everyone is watching missiles flying across the Middle East and oil prices surging toward $100 a barrel, something extremely troubling is happening inside the financial system that directly affects retirement savings across the United States.

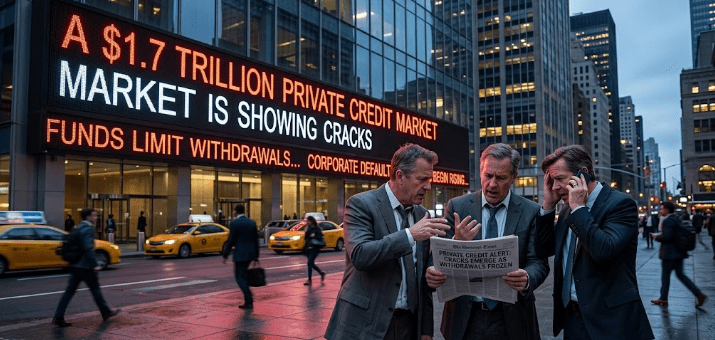

A $33 billion private credit fund managed by Cliffwater just told investors they could not withdraw their money.

Investors asked to redeem 14% of the fund’s shares. The fund capped withdrawals at 7%.

In other words, investors wanted their money back and the fund only allowed them to take half.

This was not an isolated incident.

At the same time Morgan Stanley restricted withdrawals from its $7.6 billion North Haven Private Income Fund after investors attempted to redeem 10.9% of the fund in a single quarter. The fund allows redemptions of only 5% per quarter, so a large portion of investors were denied access to their cash.

Private Credit's Margin Call Moment Arrives As Morgan Stanley, Cliffwater Gate Investors https://t.co/OoItpUchGy

— zerohedge (@zerohedge) March 12, 2026

Only about $169 million was actually paid out, which represented roughly 45.8% of the money investors requested.

And another major player is also tightening conditions. JPMorgan has been scaling back parts of its private credit lending activity as risks inside the market increase.

These numbers matter because of the size of the system we are talking about.

The global private credit market has grown to roughly $2 trillion. Just fifteen years ago it barely existed at scale.

Now it is deeply embedded across the financial world.

Major asset managers have poured enormous sums into this sector. BlackRock alone manages about $10 trillion in assets, and a significant share of institutional portfolios now includes private credit investments.

Those institutional investors include pension funds, retirement funds and large investment pools that sit behind millions of ordinary workers.

State pensions allocate billions to private credit funds.

Corporate retirement plans allocate billions to private credit funds.

Even many target date retirement funds that appear “balanced” or “diversified” hold indirect exposure through institutional investment pools.

And private credit is fundamentally different from publicly traded markets.

If you own a stock you can sell it immediately.

If you own a bond traded on the open market you can usually sell it within seconds.

Private credit does not work that way.

The loans inside these funds are made directly to companies and they are not traded on public exchanges. When investors want their money back the fund cannot simply press a button and sell the assets.

Instead the fund decides if and when withdrawals are allowed.

That is why redemption limits exist.

Most funds cap withdrawals at 5% to 10% of assets per quarter to prevent sudden runs.

When redemption requests exceed those limits the fund blocks the rest.

Which is exactly what just happened.

Investors requested 14% from the Cliffwater fund.

They were allowed 7%.

Investors requested 10.9% from the Morgan Stanley fund.

They were allowed 5%.

These restrictions appear when investors start rushing for the exits faster than funds can liquidate assets.

And historically that is one of the earliest warning signals that stress is building inside the financial system.

Many of the companies that borrowed through private credit carry extremely high debt loads. Some loans were issued at leverage ratios of six to eight times annual earnings, which looked manageable when interest rates were near zero.

Today the environment is completely different.

The Federal Reserve raised interest rates from near zero in 2021 to more than 5%, dramatically increasing borrowing costs across the economy.

Corporate bankruptcies have already surged, rising roughly 30% in the United States last year and reaching the highest level since the years following the financial crisis.

If defaults accelerate, the loans sitting inside these funds could quickly lose value.

And when that happens the funds cannot easily sell the assets to raise cash.

That is when redemption restrictions start to appear.

Financial crises rarely begin with dramatic headlines.

They begin quietly.

Funds limit withdrawals.

Investors grow nervous.

Redemption requests increase.

Assets are sold at lower and lower prices.

Credit becomes harder to obtain.

Markets begin to fall.

During the last major financial crisis the S&P 500 eventually plunged 57% from peak to bottom.

Millions of people saw retirement accounts collapse in value and many workers who expected to retire were forced to stay in the workforce for years longer than planned.

Right now we are seeing the first stage of stress emerging in a market that has grown to $2 trillion and that is heavily intertwined with pension funds and institutional portfolios.

And it is happening at the same time the world is dealing with war in the Middle East, volatile energy markets and renewed inflation pressure.

Most people are focused on the geopolitical crisis.

Very few are paying attention to what is quietly unfolding inside the financial system.

But when multiple large funds begin restricting withdrawals at the same time, it is usually a signal that something deeper is starting to break beneath the surface.

Nobody is telling you how FUCKED the financial system actually is right now.

And it started cracking TODAY.

Step 1 → JPMorgan just marked down its private credit loans and RESTRICTED lending to private credit funds.

Step 2 → Morgan Stanley is now BLOCKING redemptions at its…

— SungHoon Lee, IQ 276 (@sungleeiq) March 12, 2026