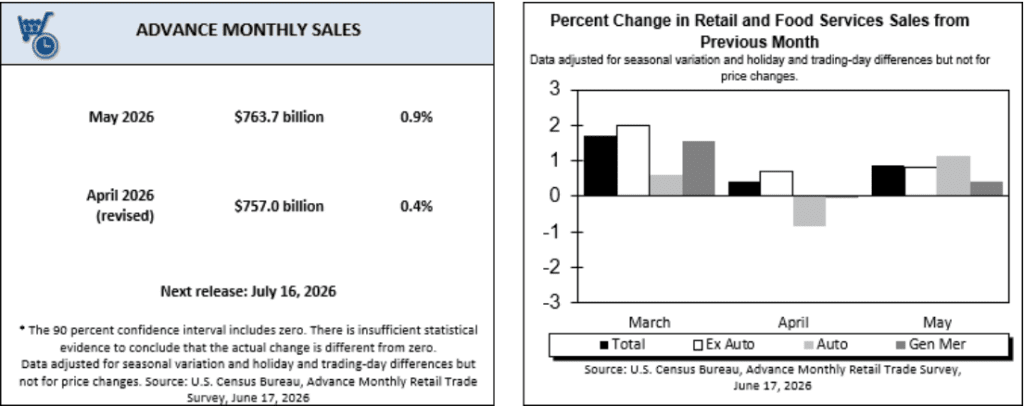

That 0.9% jump in May retail sales grabbed the headlines.

But if you zoom out, the picture looks a lot less impressive.

Earlier this year, retail sales were crawling along with 0.2% gains or barely moving at all. One stronger month doesn’t erase the fact that a lot of households have been slowing down for months.

Now look at what else is happening.

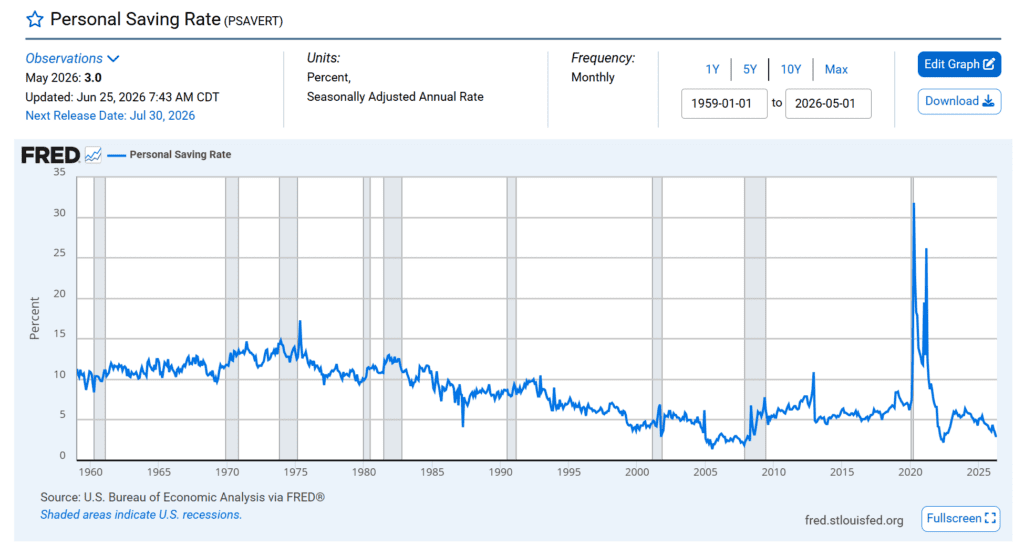

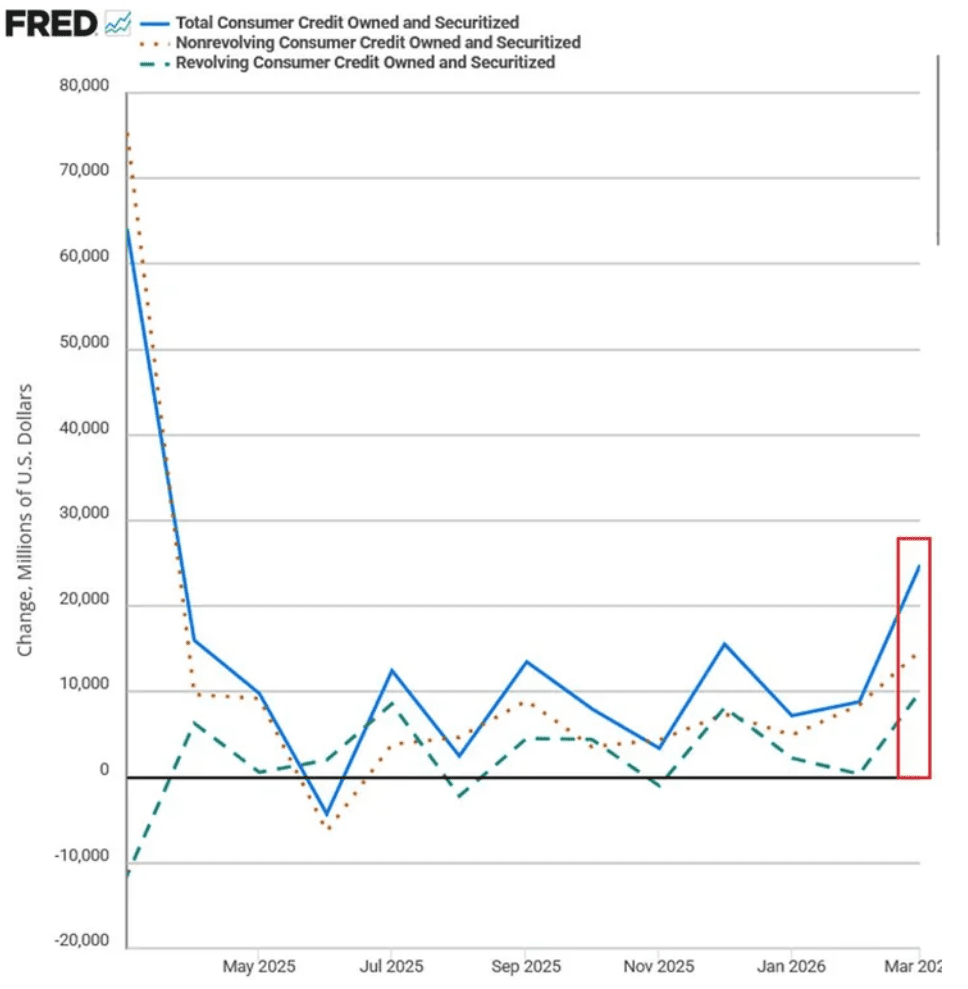

Credit card debt is sitting near a record $1.25 trillion. The savings rate is stuck around 2.6% to 3.0%, leaving many families with almost no financial cushion. Credit card defaults, especially among subprime borrowers, keep rising, and major retailers are issuing more cautious outlooks instead of celebrating a spending boom.

That’s not the backdrop you expect if consumers are in great shape.

The pattern seems pretty clear. Higher income households are still spending, which keeps the headline numbers from falling apart. Meanwhile, lower income families are cutting back on clothes, entertainment, and other discretionary purchases just to keep up with everyday bills.

That’s why so many people feel disconnected from the upbeat economic headlines. The averages can look fine even while a growing share of households feels tapped out.

Store closures haven’t turned into a nationwide wave yet, but retailers are clearly preparing for slower demand rather than stronger demand. That tells you where they think this is headed.

The question now isn’t whether consumers can keep spending.

It’s how much longer they can keep borrowing before the stronger headline numbers start catching up with what’s already happening underneath.

https://www.census.gov/retail/sales.html (official retail sales data)

https://www.newyorkfed.org/newsevents/news/research/2026/20260512 (NY Fed household debt report)

https://fred.stlouisfed.org/series/PSAVERT (savings rate data)

https://www.cnbc.com/2026/05/12/new-york-fed-credit-card-debt-stands-at-1point25-trillion.html (credit card debt details)