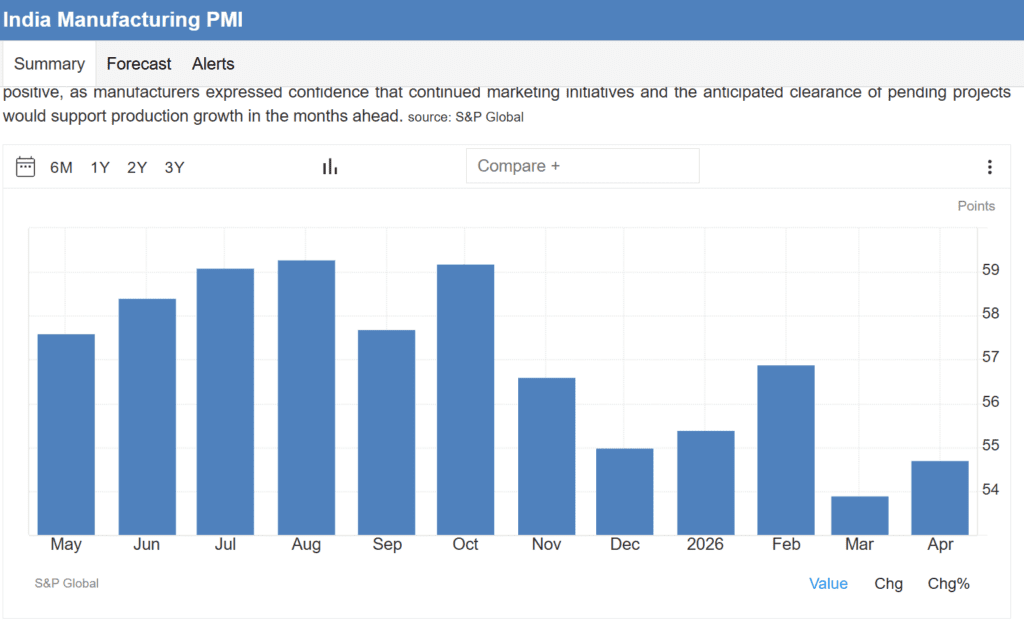

The HSBC factory index climbed to 54.7 in April, but the celebration is muted, the Iran war has officially turned global production into a cost-push nightmare…

Input costs are rising at the second-fastest rate in four years, the shipping blockade is forcing firms to choose between eating the bill or passing it to the consumer…

New orders and output grew moderately, but survey participants cited “client hesitancy” in approving pending quotes, the high-octane 2026 growth is hitting a wall of war-time reality…

Job creation hit a 10-month high as firms prepare for a potential expansion, but competitive pressures are razor-sharp, the “resilience” of the sector is being tested daily…

The factory floor is busy, but the profit margins are bleeding into the fuel tank.

A 54.7 reading is a pulse, but the input cost spike is a heart attack for small manufacturers.

If the Strait doesn’t open soon, “resilience” will be replaced by “redundancy” by the third quarter.

Revised down from 55.9 (Flash); remains near 4-year lows

Fastest rise in costs since Aug 2022; driven by energy and metal spikes

Firms are hiring for capacity, but labor costs are adding to the squeeze.

Firms starting to pass costs to consumers as they hit the “margin wall”.