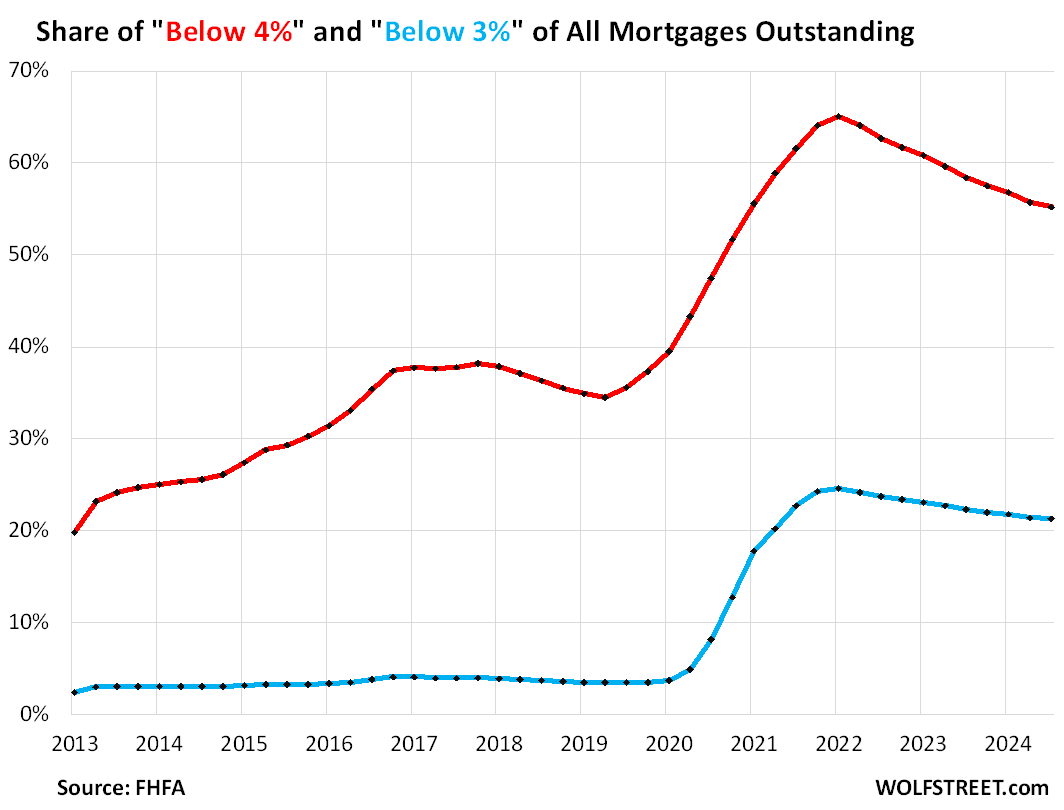

The share of mortgages outstanding with rates below 3% – as close to free money as regular folks could get – has been declining slowly but steadily to 21.3% of all mortgages outstanding at the end of Q3 2024, from the peak in Q1 2022 (24.6%), according to the Federal Housing Finance Authority’s National Mortgage Data Base of all mortgages (blue in the chart below).

The share of mortgages with rates below 4% has dropped to 55.2% of all mortgages outstanding at the end of Q3 2024, from the high of 65.1% in Q1 2022 (red). This is the share of the total number of mortgages outstanding, not of mortgage balances.

The share of adjustable-rate mortgages dropped to just 2.3% of all mortgages outstanding in Q3, after the spike in interest rates pushed the adjustable rates higher (from a share of over 10% a decade ago). Some ARMs had rates below 3% before 2020, which is why the blue line is above zero before 2020; those were ARMs. And those folks experienced a payment shock when rates began to rise in 2022.

MORE: