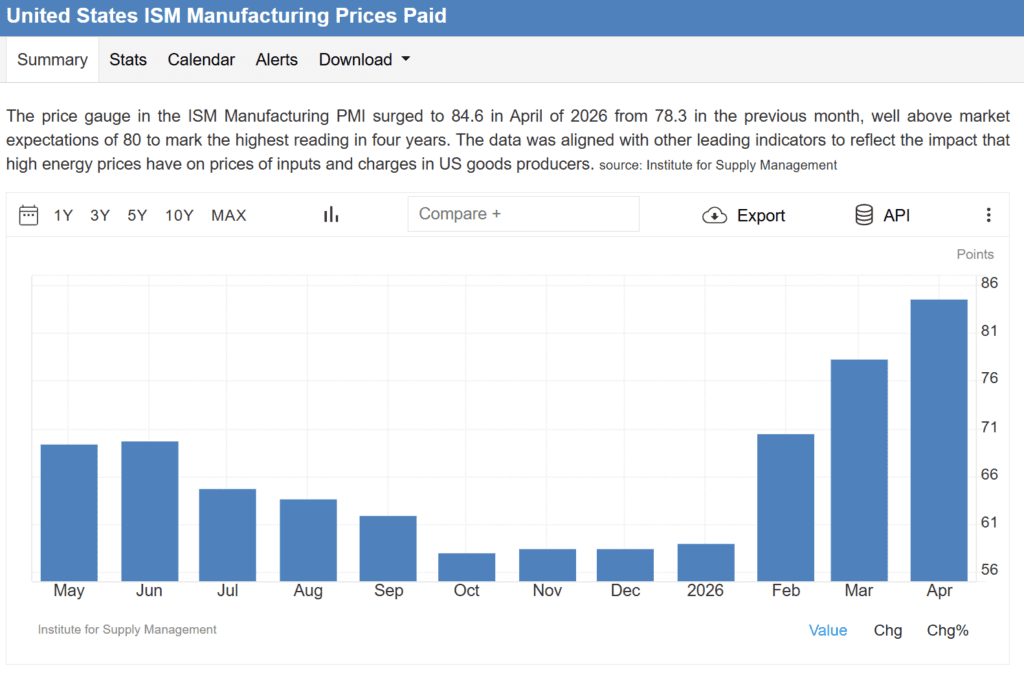

The ISM Manufacturing Prices Paid index surged to 84.6 in April (way above the expected 80 and up sharply from 78.3 in March). That’s the highest reading since April 2022 and shows input costs are rising fast again, driven heavily by energy/oil prices tied to the Middle East situation.

https://tradingeconomics.com/united-states/ism-manufacturing-prices

The overall Manufacturing PMI held steady at 52.7, exactly matching the April 1 release. While the sector is expanding, the widening gap between “output” and “input cost” is the primary concern.

https://www.forexfactory.com/calendar/252-us-ism-manufacturing-pmi

Supplier Deliveries rose to 58.9, indicating the slowest delivery times since late 2022. Logistical bottlenecks in the Middle East are cited as the primary driver for these delays.

https://economics.td.com/us-ism-manufacturing-index

Despite the inflationary print, the S&P 500 hit a new record high of 7,258, as strong tech earnings (Alphabet/Microsoft) offset the “higher for longer” interest rate anxiety.

https://www.chandlerasset.com/rates-steady-inflation-signals-persist/