The Fed just held rates steady at 3.5% to 3.75% and sounded pretty hawkish.

No rush to cut.

Inflation still matters.

Higher-for-longer remains the message.

So far, pretty straightforward.

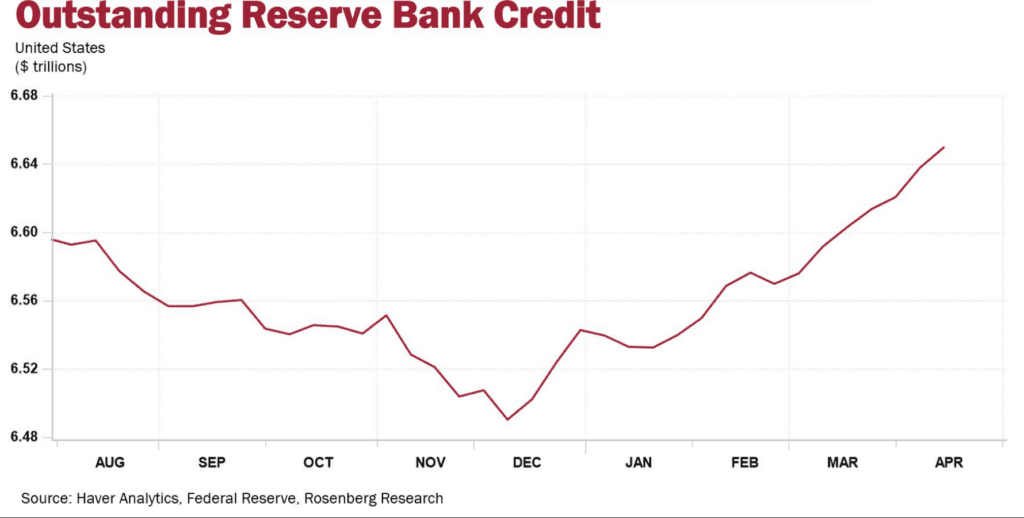

Then I looked at the balance sheet.

According to David Rosenberg, the Fed’s balance sheet has been growing at roughly a 10% annualized rate over the last four weeks.

The balance sheet is now back above $6.7 trillion.

And that’s where the debate starts.

Because if the Fed is adding liquidity through reserve management operations while keeping rates unchanged, some investors see that as easing through a different door.

Not a rate cut.

Not official QE.

But still more liquidity entering the system.

The interesting part is what happened next.

Stocks rallied.

Risk assets rallied.

The market acted more like money was getting easier, not tighter.

Now, critics of this view will point out that reserve management purchases are not the same thing as a full QE program.

And the Fed would likely argue these operations are about keeping markets functioning smoothly, not stimulating asset prices.

That’s a fair point.

But I can also understand why investors are looking at a $6.7 trillion balance sheet, a 10% annualized growth rate, and a strong market rally and asking:

If policy is truly restrictive, why is the balance sheet growing again?

That’s the question.

Not whether this is secretly QE.

Not whether the Fed is lying.

Just why the official message sounds hawkish while liquidity appears to be moving in the opposite direction.

Because if markets keep rising while rates stay high, investors may start paying more attention to what the Fed is doing than what the Fed is saying.