This NYU paper [Why do banks invest in MBS? (March 2023)] says rising interest rates have led to unrealized bank loan losses of about $1.7 trillion which is only slightly less than total bank equity capital of about $2.2 trillion.

Interest rate risk beyond MBS: The estimated losses on securities are only part of the total unrealized losses banks suffered from the rise in interest rates. Loans, like securities, also lose value when interest rates go up. Total loans plus securities as of December 2022 was $17.5 trillion. Applying the average duration of loans and securities (3.9 years), the total unrealized losses on total bank credit as of December 2022 is $17.5 × 3.9 × 2.5% = $1.7 trillion. This is only slightly less than total bank equity capital of $2.1 trillion in 2022. Hence, the losses from the interest rate increase are comparable to the total equity in the entire banking system.

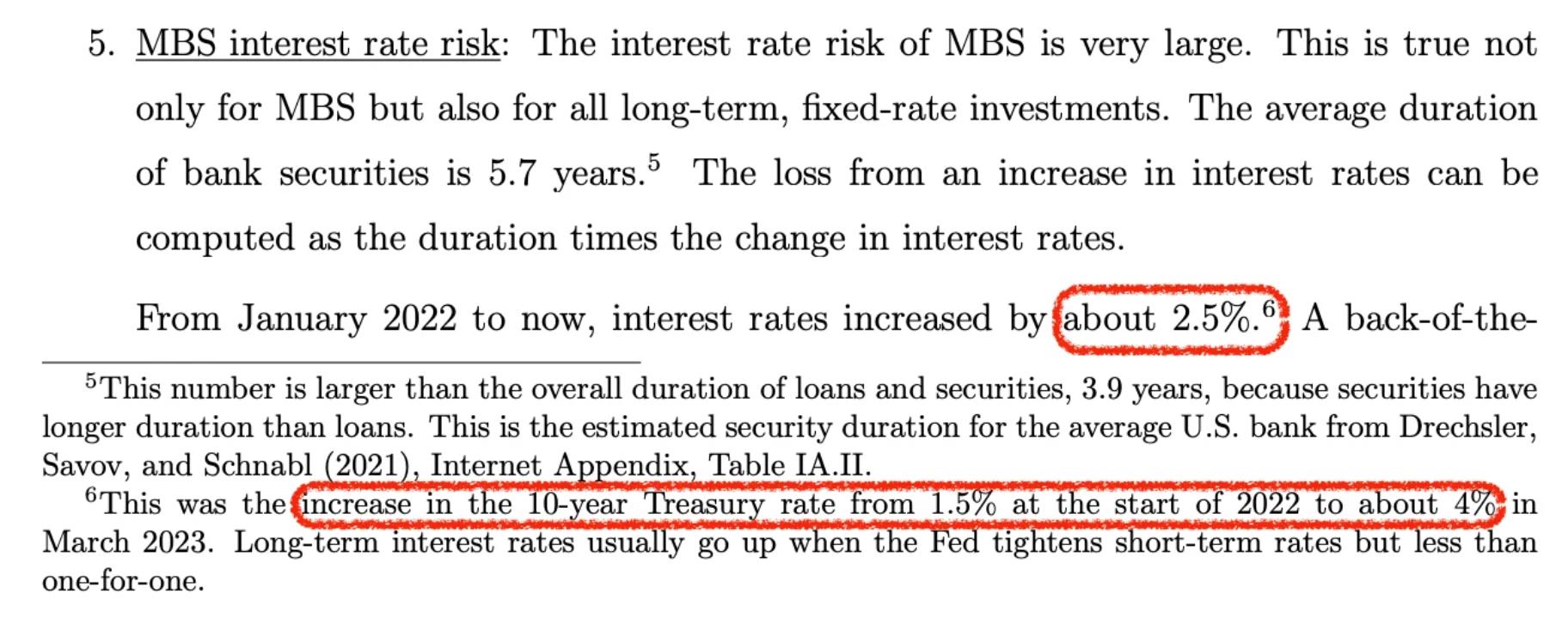

That estimate is based on the 2.5% increase in 10 year Treasury rate from ~1.5% to ~4.0% in March 2023 (footnote 6).

FRED keeps track of Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity which shows the 10 Year is now about 1/5% (0.2%) higher. Unrealized losses go up as rates go up.

Which is why the Federal Reserve created the Bank Term Funding Program (BTFP) to let banks swap devalued loan assets for full cash value to keep the banks afloat.

It just keeps going up… Bank Term Funding Program usage above $100B for the 12th consecutive week ($107.386B vs $107.242B 8/17). An over reliance on central bank funding that is growing faster than the rate of inflation, BTFP is a moral hazard!

| Date | Bank Term Funding Program (BTFP) | Up from 3/15, 1st week of program ($ billion) |

|---|---|---|

| 3/15 | $11.943 billion | $0 billion |

| 3/22 | $53.669 billion | $41.723 billion |

| 3/29 | $64.403 billion | $52.460 billion |

| 3/31 | $64.595 billion | $52.652 billion |

| 4/5 | $79.021 billion | $67.258 billion |

| 4/12 | $71.837 billion | $59.894 billion |

| 4/19 | $73.982 billion | $62.039 billion |

| 4/26 | $81.327 billion | $69.384 billion |

| 5/3 | $75.778 billion | $63.935 billion |

| 5/10 | $83.101 billion | $71.158 billion |

| 5/17 | $87.006 billion | $75.063 billion |

| 5/24 | $91.907 billion | $79.964 billion |

| 5/31 | $93.615 billion | $81.672 billion |

| 6/7 | $100.161 billion | $88.218 billion |

| 6/14 | $101.969 billion | $90.026 billion |

| 6/21 | $102.735 billion | $90.792 billion |

| 6/28 | $103.081 billion | $91.138 billion |

| 7/5 | $101.959 billion | $90.016 billion |

| 7/12 | $102.305 billion | $90.362 billion |

| 7/19 | $102.927 billion | $90.984 billion |

| 7/26 | $105.078 billion | $93.155 billion |

| 8/2 | $105.684 billion | $93.741 billion |

| 8/9 | $106.864 billion | $94.921 billion |

| 8/16 | $107.242 billion | $95.299 billion |

| 8/23 | $107.386 billion | $95.443 billion |