Something about the IRA contribution limit feels a little strange when you look back at where it started.

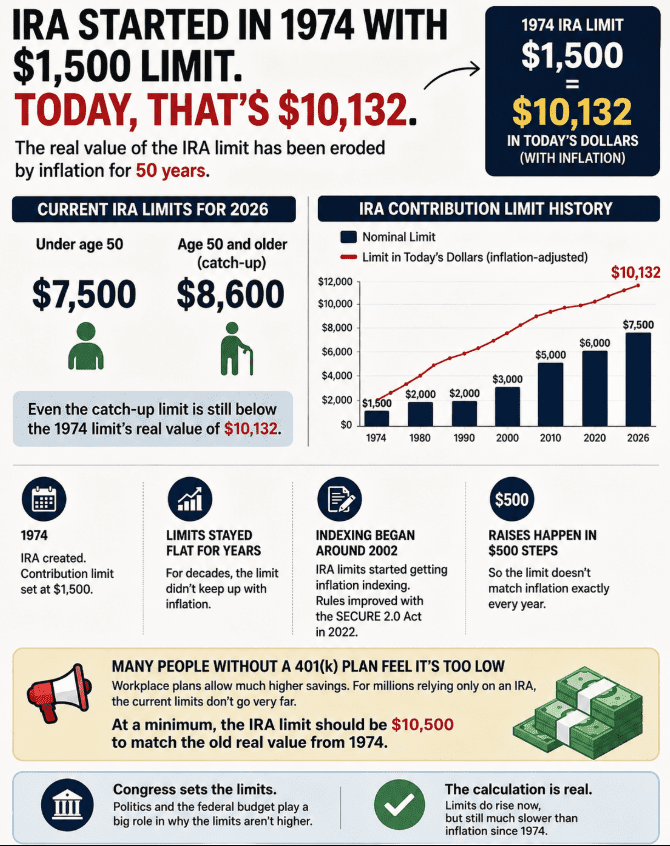

When the IRA was created in 1974, the contribution limit was $1,500.

That sounds small today, but here is the interesting part: adjusted for inflation, that $1,500 would be roughly $10,132 today.

The current 2026 IRA contribution limit is $7,500 for people under age 50 and $8,600 for those 50 and older with the catch-up contribution.

So yes, the limit has increased. It is not frozen at the 1974 number. But compared with the original purchasing power, the gap is still there.

The rules are a little more complicated because IRA limits started getting inflation adjustments around 2002, and the increases happen in $500 steps. That means the number does not perfectly track inflation every single year.

Then came the SECURE 2.0 Act of 2022, which improved some retirement rules, but the basic question remains:

Why is the amount people can put into an IRA still so limited compared with workplace retirement plans?

For someone with a 401(k), there are much higher contribution limits. But for people without access to those plans, the IRA is often one of the main tools available to build retirement savings.

That is why some argue the limit should be closer to $10,500 just to restore the real value of the original 1974 limit.

The funny part is the math is not complicated. The debate is not really about whether the number changed. It did.

The bigger question is why Congress keeps adjusting it slowly instead of asking whether the current limit actually matches the reality of retirement costs today.

And that is where politics and budget decisions enter the picture.

The IRA was created more than 50 years ago. The money people need for retirement has changed a lot since then.

The question is whether the rules have kept up.