By Peter Reagan

There’s an old joke about the economist who drowned crossing a river that was, on average, just three feet deep.

That’s the problem with averages. They can be technically accurate and practically useless at the same time.

I thought of that joke while reading the latest inflation news – and especially the debate around new Federal Reserve Chair Kevin Warsh’s preferred way of measuring inflation.

The basic idea is simple enough. Some inflation readings are noisy. Gasoline jumps one month, airfare falls the next, food spikes because of weather, used cars swing for reasons only used-car dealers seem to understand. So some economists prefer inflation measures that “trim” the biggest price increases and the biggest price declines in order to get a clearer view of the underlying trend.

That can be useful. I don’t want to dismiss it out of hand.

But here’s the problem: We do not live in an “underlying trend.”

We live in houses or apartments. We buy groceries. We fill a gas tank. We pay utility bills. We open health insurance notices with one eye closed. We don’t get to tell the cashier, “I’m sorry, but gasoline is too volatile this month, so I’ll be excluding it from my personal cost of living.”

That’s why this week’s inflation story matters so much for families.

The Fed can trim the inflation measurement.

But it can’t trim your bills.

The inflation report gave everyone something to argue about

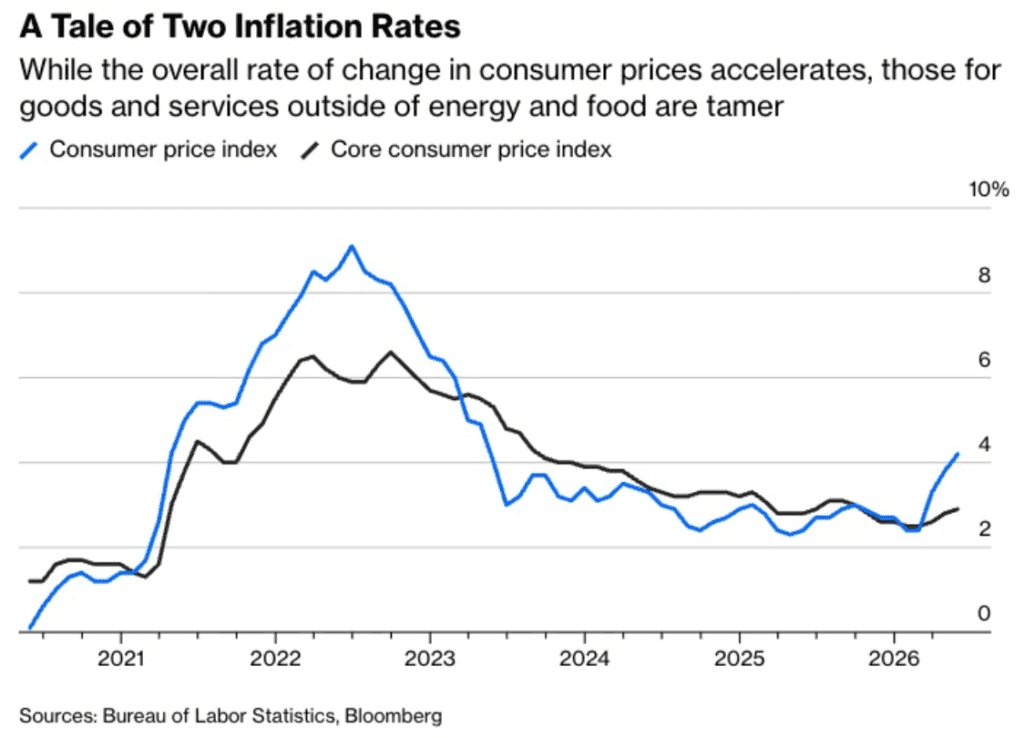

According to the Bureau of Labor Statistics (BLS), the Consumer Price Index rose 0.5% in May on a seasonally adjusted basis, bringing the annual inflation rate to 4.2%.

That is not a small number. It is more than double the Fed’s long-term 2% inflation target.

But like most economic reports, the story gets more complicated once you look under the hood.

The “core” inflation gauge – which strips out food and energy – rose just 0.2% for the month and 2.9% over the last year. That gives policymakers a little breathing room. It allows them to say, with some justification, that the broader inflation trend may not be as ugly as the headline number looks.

Bloomberg framed this as a potential “break” for Warsh as he prepares for his first Fed policy meeting. Headline inflation came in hot, but core inflation looked calmer. That gives Warsh room to argue that inflationary pressure is easing, even as everyday Americans are still absorbing a higher cost of living.

This is where I want to slow down.

Because the difference between headline inflation and core inflation is not just an economics debate. It is a real-life divide.

Food and energy are not luxuries. They are not optional. They are two of the most unavoidable categories in a household budget.

Energy rose 3.9% in May alone, according to BLS. Gasoline rose 7.0% in the month. Over the past year, energy prices rose 23.5%, while gasoline rose 40.5%.

Now imagine explaining to a retiree that inflation is not so bad once you ignore energy.

That may be statistically useful. It may even be defensible for policymakers trying to avoid overreacting to short-term price swings.

But it does not match lived experience.

And lived experience is what matters when you’re trying to make savings last through retirement.

The new debate: Should inflation get a “trim”?

Warsh has shown interest in “trimmed average” inflation measures. Investopedia explains the basic concept nicely: trimmed averages remove the prices that rise or fall the most in a given month, leaving a middle or “median” group that may provide a cleaner signal.

Again, that is not crazy.

If your doctor takes your blood pressure ten times and one reading is wildly different from the rest, maybe that reading was a mistake. Maybe your cuff slipped. Maybe you moved. Maybe the nurse had just told you how much your deductible went up.

Sometimes it makes sense to remove the outlier.

But what if the outlier is the warning?

What if the high reading is not a statistical nuisance, but the signal that something is wrong?

That is the concern with today’s inflation picture.

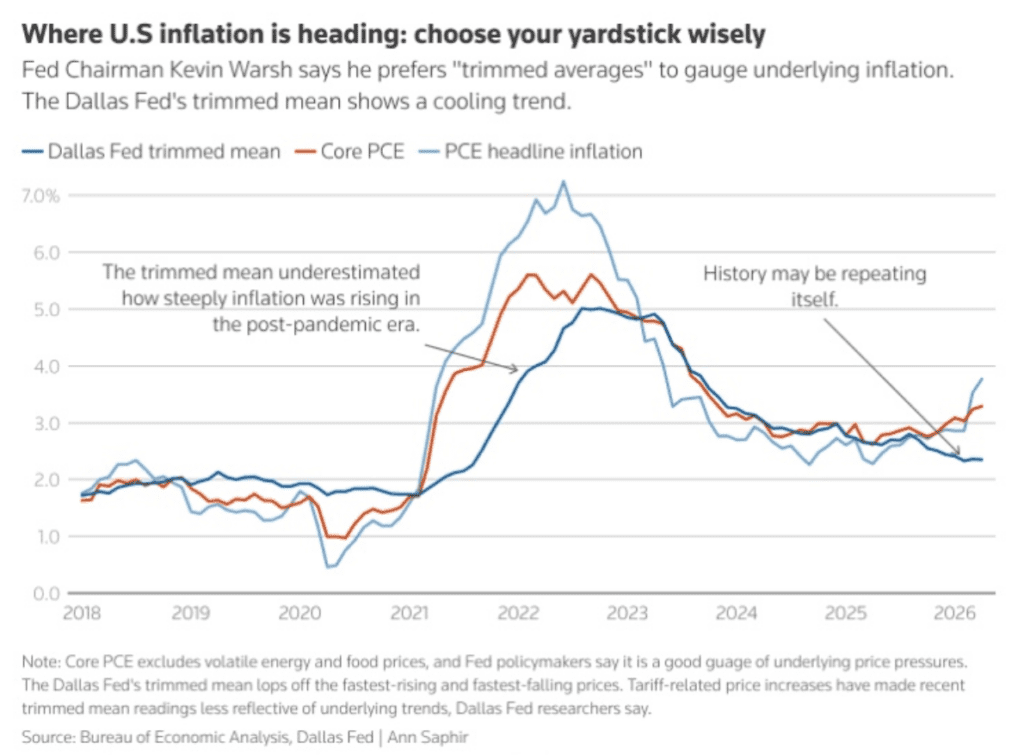

Reuters reported that the Dallas Fed’s trimmed mean PCE inflation measure – one of the best-known trimmed measures – came in at 2.3% for April, down from 2.4% in March.

That sounds encouraging. But Reuters also reported an important warning from the Dallas Fed itself: the measure may currently be understating true inflation pressure.

Why?

Because tariffs and energy shocks can push prices higher across a wide range of goods. Under normal conditions, trimming away the biggest price changes can remove noise. But if the biggest price changes are part of a broader inflation problem, trimming them away may also remove reality.

The Dallas Fed’s own page shows the gap. In April, trimmed mean PCE was 2.3%, while overall PCE inflation was 3.8% and core PCE was 3.3%.

That is a very large difference.

And it raises a question that should matter to anyone planning for retirement: Which number should you believe?

My answer is: Don’t choose just one.

Each number tells us something. Core inflation tells us something. Trimmed mean inflation tells us something. Headline CPI tells us something. CPI-W, which matters for Social Security cost-of-living adjustments, tells us something.

But the mistake is assuming the most comforting number is the most useful number.

Families feel the untrimmed version of inflation

This is where retirement savers need to pay attention.

The BLS also reported that CPI-W – the Consumer Price Index for Urban Wage Earners and Clerical Workers – rose 4.4% over the last 12 months.

That matters because Social Security cost-of-living adjustments are based on CPI-W. More specifically, the Social Security Administration calculates COLAs by comparing average CPI-W readings from the third quarter of one year to the third quarter of the next.

So May does not determine next year’s Social Security COLA by itself. July, August and September will matter most.

Still, May’s CPI-W reading is a reminder of the pressure retirees face.

Even when Social Security adjusts, it adjusts after the damage has already happened. Prices rise first. The adjustment comes later.

That delay matters.

If your utility bill jumps in May, you do not get a COLA in June. If gasoline rises 40% from a year earlier, your monthly budget absorbs the shock now. If grocery prices creep higher, you pay the higher price every week.

Inflation is experienced in real time.

Relief arrives on a schedule.

For retirees living on a fixed income, that is not an academic distinction. That is the difference between feeling comfortable and feeling squeezed.

And for near-retirees still working, the picture is not much better. BLS reported that real average hourly earnings fell 0.7% from May 2025 to May 2026.

In plain English: Wages did not keep up with prices.

That matters enormously in the final years before retirement. Those are supposed to be the years when many Americans make their last big push to strengthen their savings. Instead, inflation is eating into the very income they would otherwise set aside.

This is the quiet retirement crisis inside the inflation report.

It is not just that prices are rising.

It is that prices are rising at exactly the wrong time for people who need stability most.

Lower inflation is not the same as lower prices

There is another point that gets lost in these debates.

When economists say inflation is “cooling,” they usually mean prices are rising more slowly. They do not mean prices are falling back to where they were.

That may sound obvious, but it is one of the biggest disconnects between official commentary and household reality.

If something cost $100, then rose to $120, and then inflation slowed, that does not mean the price goes back to $100. It may simply mean the price rises to $122 instead of $126.

That is improvement in the inflation rate.

It is not relief in the price level.

This distinction is especially important for retirees because retirement planning is really purchasing-power planning. The question is not merely, “How many dollars do I have?” The question is, “What will those dollars buy over the next 10, 20 or 30 years?”

That is the uncomfortable part of inflation. It does not have to destroy purchasing power all at once. It can do its work slowly.

A few percent here. A few percent there. A grocery bill that never quite returns to normal. An insurance premium that becomes the new baseline. A utility bill that resets expectations. A restaurant meal that quietly becomes a special occasion instead of a weekly habit.

Over time, inflation does not just raise prices.

It lowers expectations.

That may be the most overlooked retirement risk in America.

The credibility problem

I want to be fair to Warsh and to the economists who study these measures.

A trimmed inflation measure can be a legitimate tool. The question is not whether it is fraudulent or useless. That would be too simplistic, and frankly, not accurate.

The better question is whether the public will trust it.

If inflation has been above the Fed’s target for years, and then policymakers start emphasizing a measure that looks cooler than the numbers households actually feel, what are regular Americans supposed to think?

They may not know the technical arguments behind trimmed mean inflation.

But they know their bills.

And when official language drifts too far from lived reality, trust breaks down.

This is the danger. Not conspiracy. Incentives.

Policymakers want flexibility. They want room to lower interest rates if they believe the economy is weakening. They want to avoid overreacting to temporary price shocks. They want to communicate confidence.

Those incentives are understandable.

But retirees have different incentives. They want their savings to last. They want predictable costs. They want to avoid being forced into difficult choices because official inflation math underestimated their real cost of living.

Those incentives matter, too.

In fact, for our readers, they matter more.

What everyday Americans should take from this

I don’t think the lesson is, “Ignore the Fed.”

The Fed matters. Inflation measurements matter. Interest-rate policy matters. These decisions shape the broader economy, the cost of doing business and financial markets, too. That’s why every news network covers every Fed meeting, every commencement speech or public address given by any of the 19 members of the Federal Open Market Committee (FOMC). The decisions they make really are important.

But the bigger lesson is this: Don’t base your financial confidence on one official number.

Especially not the most convenient one.

A serious retirement plan has to account for the possibility that inflation remains sticky, uneven and personally painful even when certain measures look calmer. It has to account for the fact that healthcare, housing, insurance, food and energy may not behave like a neat average. It has to account for the risk that purchasing power erodes faster than policymakers expect.

That is why diversification matters.

Not because anyone can predict the next CPI report. Not because physical gold or precious metals guarantee any particular outcome. (They don’t.)

But because physical precious metals have historically served a safe-haven role far different from paper promises and debt-based assets. Gold does not depend on a committee deciding which inflation measure is most appropriate this month. It does not need the Fed to define purchasing power correctly in order to retain its appeal as a long-term store of value.

That is not speculation. It is a recognition of history.

When official money loses purchasing power, people tend to rediscover why physical gold has mattered for thousands of years.

The bill still comes due

The most important inflation number is not the one policymakers prefer.

Often, the most important number is printed at the bottom of your grocery receipt.

Or on your electric bill.

Or at the gas pump.

Or in the Social Security notice that arrives months after prices have already gone up.

So yes, economists can debate whether CPI, PCE, core PCE, CPI-W, median inflation or trimmed mean inflation gives the cleanest policy signal.

That debate does matter. But it does not pay the bills.

For families, the question is much more practical:

Will my savings still buy what I need them to buy?

If the answer is uncertain, then it may be time to look beyond official reassurance and think seriously about diversification. Physical precious metals are not a magic solution. But for many Americans concerned about inflation, currency weakness and retirement purchasing power, they remain a sensible subject for education and consideration.

The Fed can trim the measurement.

You and I still have to pay the full price.