After shattering 30 all-time high price records, global demand for gold also hit an all-time high this year. Is massive demand causing record high prices? Or are high prices causing fear of missing out? Let’s dive into the forces behind record gold demand…

Your News to Know rounds up the most important stories about precious metals and the overall economy. This week, we’ll cover:

- Gold demand hits $100 billion for the first time ever

- Election year is good for gold regardless of the results

- Something is amiss in the inflation readings…

- …should we believe them or not?

Gold demand sets new record over $100 billion

As the World Gold Council noted in a recent report, gold demand recently passed $100 billion, and almost nobody noticed. Well, Bloomberg did. And the Financial Times is paying attention.

Central banks haven’t broken the previous year’s record (officially, that is), purchases are tracking 2022 levels. Total gold demand increased 5% year-over-year, which is no small development! Total gold demand for the third quarter came in at 1,313 metric tons – or 42,214,000 troy oz.

If demand continues this way, we’ll have to start asking where the gold is coming from.

Despite record demand, sales of gold coins and bullion bars remains subdued. Jewelry demand has declined as well – suffering from high prices, I assume. Now, for jewelry this makes sense – that $1,000 ring you were looking at now costs $1,400? You might reconsider. Investment gold, though, we expect to be price insensitive. When the price of gold bullion goes up, we’re mostly seeing loss of currency purchasing power.

With this in mind, who pushed gold demand past this landmark figure the most?

Here’s my list of suspects, with most influential at the top. This is mostly an intellectual exercise, though – demand is so strong and broad-based, one source of demand isn’t necessarily more or less important than the others:

- Central banks from around the world (but mostly emerging markets)

- Chinese and Indian gold buyers, who have kept buying despite sky-high premiums, dealer scams and government incentives against physical gold ownership

- Speculators who seemingly appeared out of nowhere and started buying gold by the billions

- Middle Eastern consumers who are using gold to flee from destroyed currencies

- Vietnamese consumers, who have formed an informal trading network because the official one wasn’t cutting it

Who’s missing on this list?

It’s mostly the Western gold investor. Here in the West, it’s somehow considered impolite or old-fashioned to buy gold bullion. Meanwhile, everone else in the world diversifies with physical precious metals as a matter of course. Why wouldn’t you?

Why this divide? I have some theories – basically they boil down to this: If you haven’t lived through a true financial crisis, the benefits of owning physical precious metals might not be as clear to you. The more recently you’ve been confronted with financial ruin, the more likely you are to see the benefits of owning tangible assets.

I don’t doubt that Western investors will return to the gold market. Obviously, that will contribute even more to demand. But I do wonder how many more ounces their money would’ve bought had they made their move sooner rather than later.

Here’s why either candidate’s win is good news for gold

The thing every gold investor no doubt wants to know is how gold will fare in the upcoming four-year tenure. Donald Trump and Kamala Harris are mostly on the opposing side of rhetoric, as was the case during Trump’s first candidacy with Hillary Clinton opposing.

Every pundit has an opinion, so we’ll focus on the hard data. We’ll start with Harris, given that she is Joe Biden’s VP and has arguably grabbed the reins as Biden’s term in office draws to a close.

Whether we blame supply chain snarls, the Fed’s absurdly slow pace of interest rate hikes or the trillions and trillions of deficit spending flooding the economy, Biden’s presidency will be remembered for historic inflation. That obviously helped send gold to its current levels.

The analysis I linked to above claims that a Harris presidency would be less inflationary than that of Trump. It’s not exactly clear why that would be the case… Harris has sworn to back massive spending on nearly every front, from small businesses to first-time homebuyers.

You personally might not benefit from these pork barrel programs, but dollars to fund them will be printed nonetheless. And we know what that means for the price of gold.

What about a second Trump term? Well, Trump has always often gone on record wanting a weaker dollar. A weaker dollar makes U.S. goods more affordable overseas – great for manufacturing and for exporters, not so great for everyone else. I hope you know this by now, but just in case: A weaker dollar invariably means stronger gold.

What isn’t being given nearly enough attention is that the Federal Reserve will probably continue to have an even bigger role in the dollar’s strength or weakness (regardless of who is nominated as chairman). The Fed has to cut rates. Lower interest rates means a weaker dollar and therefore higher gold price.

No amount of rhetoric can get around this issue. Today’s interest rates are still high compared to the last 24 years – and that was a period long enough that an entire economy adapted to cheap credit. In this situation, the Fed has to either keep rates high and let the dead wood, the cheap-credit-dependent malinvestments, collapse. That’s beneficial for long-term economic health – but obviously quite traumatic in the short term.

Alternately, the Fed can lower rates. Cheapen credit. Encourage dollar devaluation (and government deficits).From the recent 50-basis point cut, you know which course they’ve chosen…

One thing that analysts seem to agree on is that, regardless of the policies being passed, gold will continue its best run in 50 years. Goldman Sachs joined the growing amount of forecasters predicting $3,000 gold next year (maybe sooner). It seems those analysts remaining skeptical would do well to listen.

Inflation near 2%, yet gold soars. Who is lying here?

What’s inflation like these days? When in doubt, consult ShadowStats. But before we turn to John Williams’s insights once again, I’ll explain why we must invoke the good economist.

We’re being told that the Federal Reserve’s fight with inflation has been so successful that the base inflation rate is just 2.1%, barely above the 2% target. If that’s true, then gold has “decoupled” from inflation. Generally speaking, the argument goes like this: Gold’s price doesn’t really change – when the dollar weakens, it takes more dollars to buy the same gold. So we have to ask, if inflation is moderating, why is gold’s price still surging?

Has inflation really plunged?

That is the mainstream take, but not one supported by reality or historical precedent.

To believe gold is moving independently from inflation for perhaps the first time since 1971, you would have to be a very strong believer in the accuracy of CPI measurements. And not many seasoned economists are, whether they like to admit it or not. For example, Dr. Ron Paul told us CPI measurements were “nonsense” and it’s hard to disagree with him.

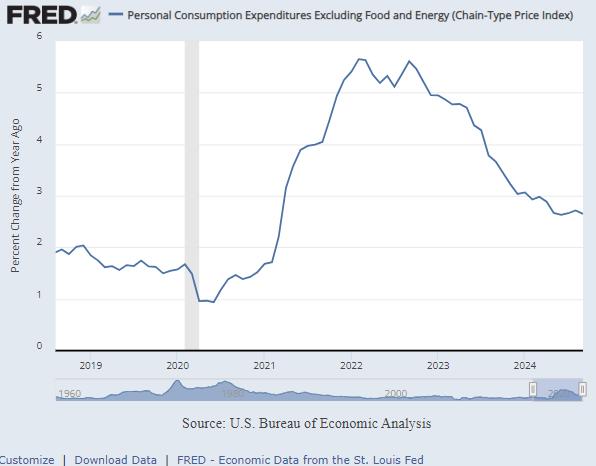

The Fed’s “preferred” measure of inflation, the Personal Consumption Expenditures (PCE) index, shows a reading of 2.7% year-on-year. It’s come down by about half from its peak back in 2022:

Can this be happening at the same time gold hits over 30 new all-time highs in less than a year?

John Williams has consistently placed core inflation between 6% and 8% since 2008, placing it closer to 15% in 2023. As his website puts it:

Have you ever wondered why the CPI, GDP and employment numbers run counter to your personal and business experiences? The problem lies in biased and often-manipulated government reporting.

Williams’ website gives a far more detailed explanation for his own gauge than anything you can expect from a government bureaucrat. Here’s why:

- Voters hate inflation! As soon as prices become a political issue, you can obviously expect massive pressure within the government bureaucracy to understate the rate of inflation.

- Social Security COLAs: Social Security is already the federal government’s #1 expense. Every 10 basis points of inflation equates to an additional billion dollars (more or less) in SS payments. So a lower official rate of inflation lowers pressure on the Social Security trust fund, which is already on the brink of bankruptcy.

- Tax collection: Inflation pushes up all prices, not just essentials like food and fuel. Rising asset prices mean bigger tax bills – so the federal government actually profits from the problem they create.

The reason it’s important to understand the incentives here is simple: We’re going to be told inflation has returned to 2% soon. We’re already being told it’s almost 2%, that it’s not a problem (and never was!) and that it wasn’t Biden’s or the Fed’s fault.

That’s an excuse for another round of monetary easing. And this could be the one that breaks the camel’s back…

In other words, expect your purchasing power to quietly and quickly evaporate – while officials assure you it’s not happening. Yes, more gaslighting ahead.

If you’re a gold investor, you’ll watch gold’s price continue making headlines while mainstream analysts scratch their heads: “Gold at $3,000 with 2% inflation? Gold’s in a bubble!”

Someone’s measure isn’t working right, and given gold’s performance, plus the incentives for under-reporting inflation numbers, I think it’s safe to listen to what Williams tells us. Gold has always been the primary method of measuring a currency’s weakness and, therefore, a nation’s true rate of inflation.

Putting too much faith in official reassurances seems as dangerous as ever right now, as another rate cut looms before the end of the year.