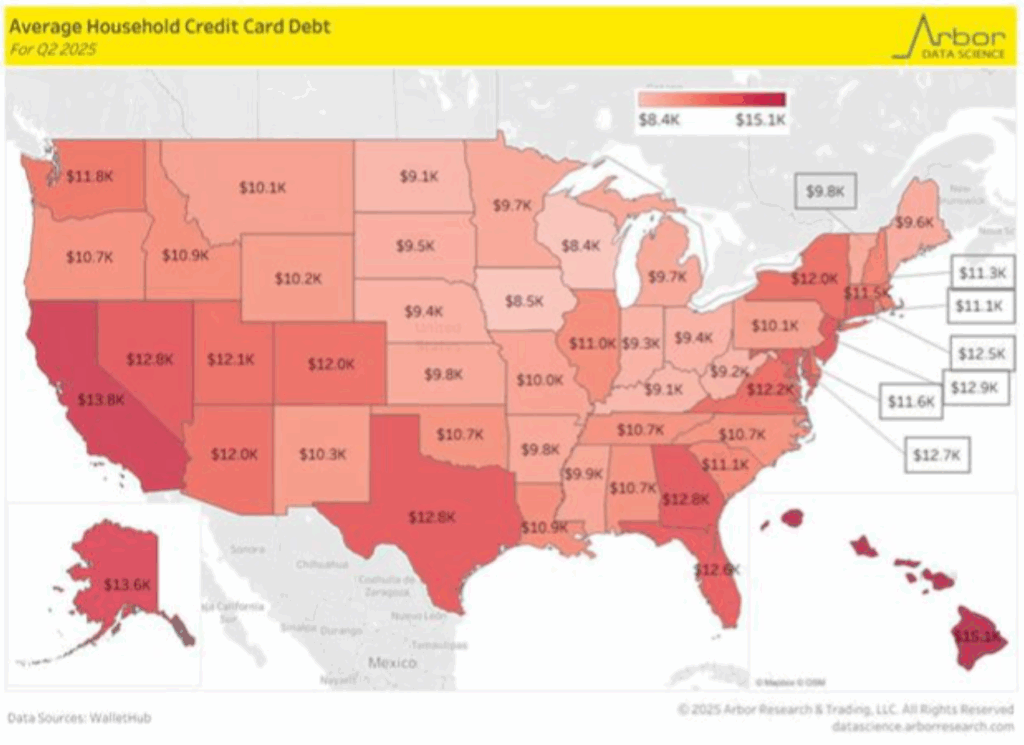

$1.33 trillion in credit card debt. That is not strength. That is panic. The average family owes $10,668. You can feel it in the lines at the grocery store, in the gas pump, in the monthly bills that never stop. Yellen says it shows “a strong consumer.” Families call it desperation.

First Brands just collapsed. That might sound like another corporate story, but it isn’t. This is a $2 trillion leveraged loan market built on rushed deals and blind hope. Investors thought spreading risk across hundreds of loans would save them. It didn’t. When First Brands fell, hundreds of slices of debt wobbled. Insurers, pension funds, banks. Everyone holding these bets just got a wake-up call.

Car loans are going off the rails. Delinquencies up 50 percent. Zions and Western Alliance are writing off loans tied to fraud in real estate. Everyday Americans are crumbling under the weight. Everything is connected. Credit cards, leveraged loans, auto loans, they are all wires in a live circuit. Touch the wrong one and the whole system sparks.

Consumers across all income categories are struggling to make their monthly car payments, with more than one in five borrowers paying more than $1,000 a month#MacroEdge

— MacroEdge (@MacroEdgeRes) October 17, 2025

Recession incoming.

Oil is a classic indicator that one’s coming. https://t.co/UfhcD8PTyz

— QE Infinity (@StealthQE4) October 17, 2025