People keep calling 2020 homebuyers geniuses.

I’m not so sure.

A lot of them were simply standing in front of one of the biggest waves of money creation in modern history.

During Covid, the Fed flooded the system with money.

M2 money supply jumped from roughly $15 trillion to more than $21 trillion in a very short period of time.

Interest rates were pushed near zero.

Trillions of dollars suddenly needed somewhere to go.

A lot of it went into assets.

Especially housing.

National home prices have surged roughly 54% since 2020.

The median home price is now above $400,000.

If you bought a house before the money printer went into overdrive, your timing could not have been much better.

But this is where the story gets twisted.

People see the gains and think the success story is the homeowner.

The real story is what happened to everyone else.

The same policies that inflated housing also inflated the cost of living across the economy.

Food costs climbed.

Insurance costs climbed.

Rent climbed.

Utilities climbed.

The basic cost of existing became more expensive.

Housing became less of a place to live and more of a speculative asset people expected to keep rising in value.

That worked great if you already owned one.

It was a disaster if you were trying to buy your first one.

Home prices rose much faster than incomes.

Down payments became harder to save.

Monthly payments exploded.

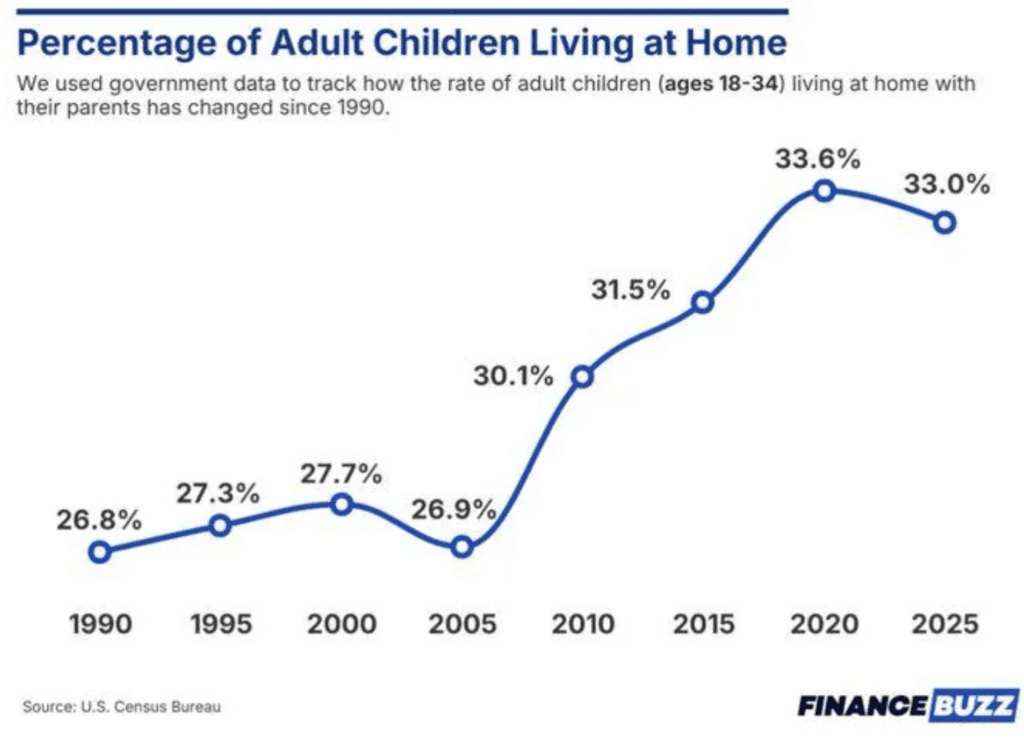

The result is visible everywhere.

The share of adult children living with their parents is near modern highs.

Many young Americans have delayed moving out, delayed buying a home, delayed marriage, or delayed starting families because the numbers simply do not work.

That is why so many people roll their eyes when they hear that inflation is cooling.

The damage was already done.

Prices do not go back to where they were just because inflation slows.

The money printer created winners.

It created losers too.

The winners got asset appreciation.

The losers got a cost of living crisis.

And both came from the same policy.