This is consistent with the effects cited in the recently released SF Fed study of 150 years of tariffs.

Tariff shocks = higher unemployment = lower inflation = clear aggregate demand contraction. This is not model based. It’s historical, empirical & statistically robust pic.twitter.com/wHbqUXofNV— Fifty Shades of Truth (@RamonGo62661955) November 15, 2025

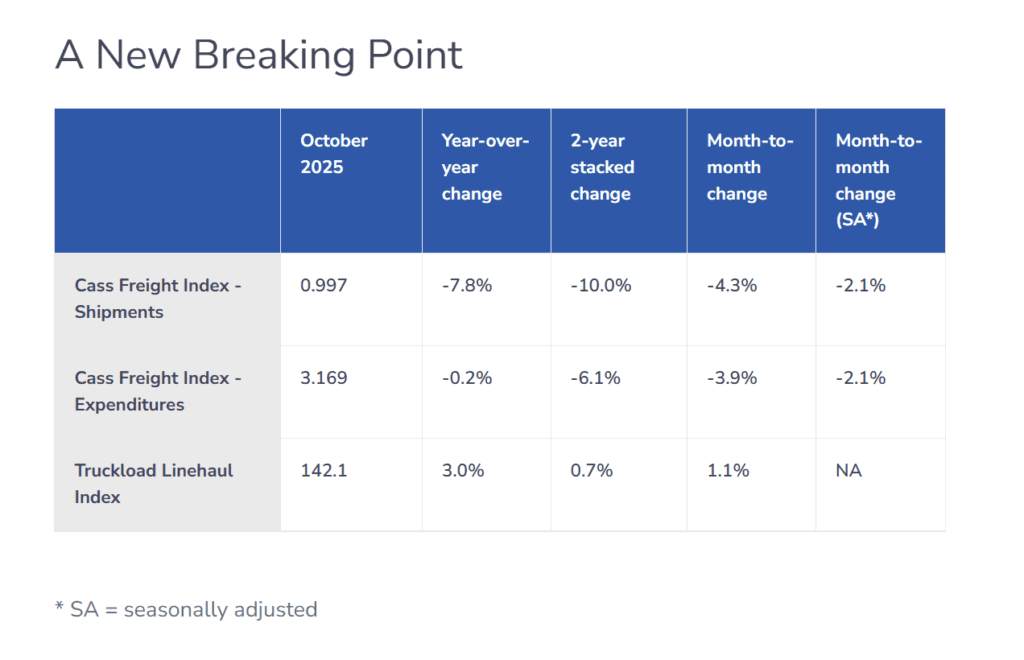

Cass Freight Index® – Shipments

- The shipments component of the Cass Freight Index fell 4.3% m/m in October, or 2.1% m/m in seasonal adjusted (SA) terms, reversing the gain in September.

- The y/y decline in shipments widened to 7.8% in October, from a 5.4% y/y decline in September.

In recent months, the declines have been concentrated in LTL, as ongoing LTL rate increases in a soft market cause more shippers to consolidate LTL loads into TLs, in addition to the insourcing going on at a pair of mega-shippers.

Demand air pockets are likely to continue, but the severity of inflation depends on the coming Supreme Court ruling on IEEPA tariffs, which could occur any time from soon to June.

- After rising 13% in 2021 and 0.6% in 2022, the index declined 5.5% in 2023 and 4.1% in 2024, and is trending toward another considerable decline in 2025.

- In November, the shipments component of the Cass Freight Index would decline 10% y/y on the normal seasonal pattern.

https://www.cassinfo.com/freight-audit-payment/cass-transportation-indexes/october-2025