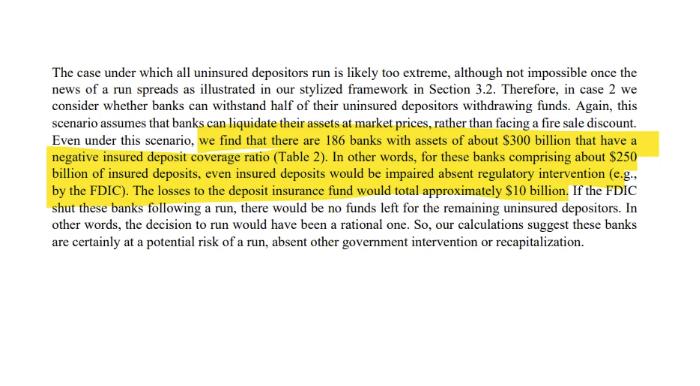

If half of uninsured depositors decide to withdraw, the losses due to CRE distress would result in up to 58 smaller regional banks becoming insolvent in addition to 186 banks that would become insolvent just due to higher rates.

Wut Mean?:

- The U.S. banking system’s market value of assets is about $2.2 trillion lower than suggested by their book-value accounting for loan portfolios held to maturity.

- Consequently, about half of U.S. banks (2,315) with $11 trillion of assets have a lower value of their assets compared to the face value of their debt liabilities.

- About half of deposits are uninsured, accounting for about $9 trillion of bank funding in the aggregate.

- If there is a widespread run by uninsured depositors, more than 1,600 banks could fail with aggregate assets of close to $5 trillion.

- The commercial real-estate distress would add up to an additional $160 billion of losses and a $2.2 trillion decline in the value of bank assets due to higher rates.

- While losses due to commercial real estate distress are an order of magnitude smaller than the decline in bank asset values associated with a recent rise of interest rates, they would impact a sizable set of banks.

- Due to these losses, up to 580 additional banks with aggregate assets of $1.2 trillion would have their mark-to-market value of assets below the face value of all their non-equity liabilities.

- Consequently, about half of U.S. banks (2,315) with $11 trillion of assets have a lower value of their assets compared to the face value of their debt liabilities.

Remember, higher interest rates put pressure on commercial real estate–especially on deals financed with debt at historically high property values and low interest rates.

Many of these loans mature in the next couple of years and some are going to have to try and refinance at much higher rates–the firms on the other end of these loans ARE NOT on a solid foundation to do so:

https://www.reddit.com/r/Superstonk/comments/14hc7pk/the_share_of_nonfinancial_firms_in_financial/

{kind=link}

https://www.reddit.com/r/Superstonk/comments/14uh1ts/the_debt_time_bomb_is_ticking_rising/

{kind=link}

On top of this, as this month, just half of U.S. workers had returned to the office compared to pre-pandemic levels–paying a ton of money for empty space.

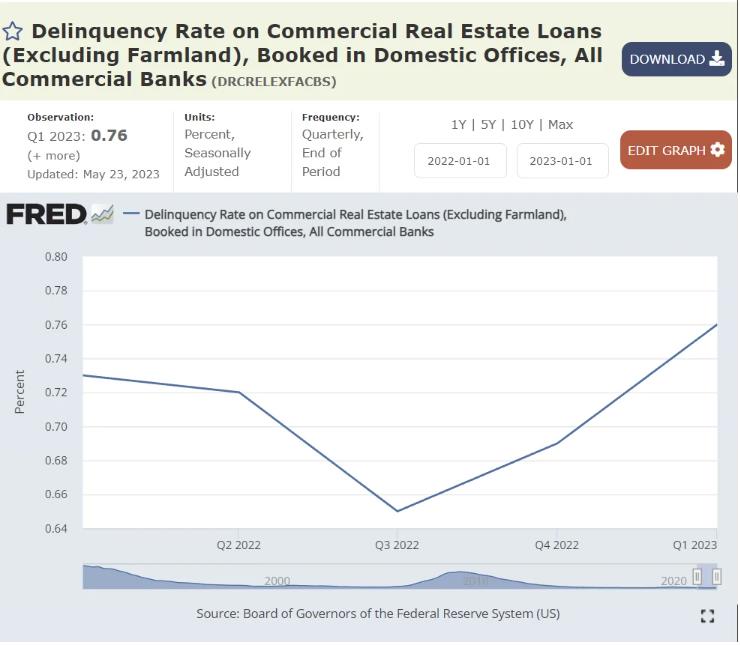

In the first quarter of 2023, the office vacancy rate reached 18.6%, 5.9% higher then the last quarter of 2019.

REITs focused on the office sector declined by about 60% since the beginning of pandemic, implying more than 30% decline in the value of their office buildings.

While the overall delinquency rate on commercial mortgages is still relatively low, it has been quickly rising, especially in the office sector.

For example, PIMCO and Blackstone recently defaulted on office loans.

The Outlook is not good either:

July 2023 Senior Loan Officer Opinion Survey on Bank Lending Practices. Banks plan to further tighten lending standards across all loan types:

- Banks tightened standards for all CRE loan categories, with both large and other banks showing similar tightening levels.

- Demand for CRE loans weakened, with other banks seeing a greater decline than large banks. Foreign banks also reported a decrease in demand and tighter standards.

- A majority expect stricter standards for construction and nonfarm loans, with a sizable portion also expecting tightening for multifamily property loans.

- Reasons for the expected tightening include:

- Uncertain economic outlook.

- Expected decline in the value of collateral.

- Anticipated decrease in credit quality.

- Reduced risk tolerance.

- Predicted liquidity challenges.

- Concerns about funding costs, deposit outflows* &, and potential impacts of legislative or supervisory changes.

{kind=link}

Bank Term Funding Program (BTFP):

https://fred.stlouisfed.org/series/H41RESPPALDKNWW

{kind=link}

| Date | Bank Term Funding Program (BTFP) | Up from 3/15, 1st week of program ($ billion) |

|---|---|---|

| 3/15 | $11.943 billion | $0 billion |

| 3/22 | $53.669 billion | $41.723 billion |

| 3/29 | $64.403 billion | $52.460 billion |

| 3/31 | $64.595 billion | $52.652 billion |

| 4/5 | $79.021 billion | $67.258 billion |

| 4/12 | $71.837 billion | $59.894 billion |

| 4/19 | $73.982 billion | $62.039 billion |

| 4/26 | $81.327 billion | $69.384 billion |

| 5/3 | $75.778 billion | $63.935 billion |

| 5/10 | $83.101 billion | $71.158 billion |

| 5/17 | $87.006 billion | $75.063 billion |

| 5/24 | $91.907 billion | $79.964 billion |

| 5/31 | $93.615 billion | $81.672 billion |

| 6/7 | $100.161 billion | $88.218 billion |

| 6/14 | $101.969 billion | $90.026 billion |

| 6/21 | $102.735 billion | $90.792 billion |

| 6/28 | $103.081 billion | $91.138 billion |

| 7/5 | $101.959 billion | $90.016 billion |

| 7/12 | $102.305 billion | $90.362 billion |

| 7/19 | $102.927 billion | $90.984 billion |

| 7/26 | $105.078 billion | $93.155 billion |

https://www.reddit.com/r/Superstonk/comments/11prthd/federal_reserve_alert_federal_reserve_board/

{kind=link}

- Association, or credit union) or U.S. branch or agency of a foreign bank that is eligible for primary credit (see 12 CFR 201.4(a)) is eligible to borrow under the Program.

- Banks can borrow for up to one year, at a fixed rate for the term, pegged to the one-year overnight index swap rate plus 10 basis points.

- Banks have to post collateral (valued at par!).

- Any collateral has to be “owned by the borrower as of March 12, 2023.”

- Eligible collateral includes any collateral eligible for purchase by the Federal Reserve Banks in open market operations.

Richard Ostrander (one of the architects of BTFP) spoke about it the other day:

The Fed has created an emergency backstop program so that banks won’t have to sell assets into the market if customers pull deposits in search of more attractive yields for their savings….

{kind=link}

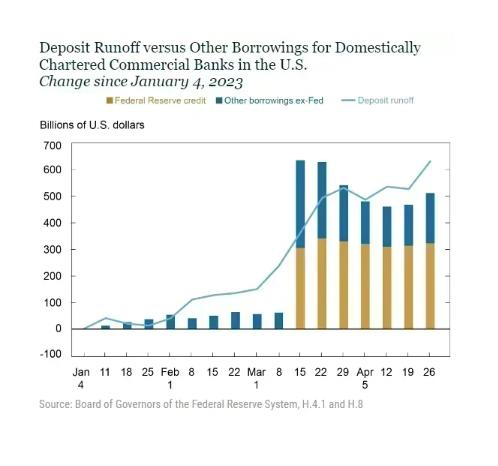

Over the few weeks prior to the FDIC receivership announcements on March 10 and 12, the banking sector lost another approximately $450 billion. Throughout, the banking sector has offset the reduction in deposit funding with an increase in other forms of borrowing which has increased by $800 billion since the start of the tightening.

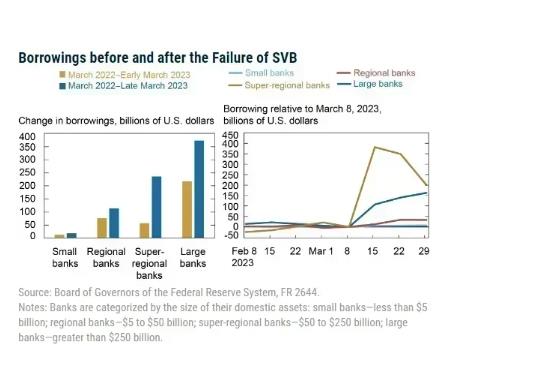

The right panel of the chart below summarizes the cumulative change in deposit funding by bank size category since the start of the tightening cycle through early March 2023 and then through the end of March. Until early March 2023, the decline in deposit funding lined up with bank size, consistent with the concentration of deposits in larger banks. Small banks lost no deposit funding prior to the events of late March. In terms of percentage decline, the outflows were roughly equal for regional, super-regional, and large banks at around 4 percent of total deposit funding:

The blue bar in the left panel above shows that the pattern changes following the run on SVB. The additional outflow is entirely concentrated in the segment of super-regional banks. In fact, most other size categories experience deposit inflows.

The right panel illustrates that outflows at super-regionals begin immediately after the failure of SVB and are mirrored by deposit inflows at large banks in the second week of March 2022.

Further, while deposit funding remains at a lower level throughout March for super-regional banks, the initially large inflows mostly reverse by the end of March. Notably, banks with less than $100 billion in assets were relatively unaffected.

- Large banks increased borrowing the most, which is in line with deposit outflows being strongest for larger banks before March 2023.

- During March 2023, both super-regional and large banks increase their borrowings, with most increases being centered in the super-regional banks that faced the largest deposit outflows.

- Note, however, that not all size categories face deposit outflows but that all except the small banks increase their other borrowings.

- This pattern suggests demand for precautionary liquidity buffers across the banking system, not just among the most affected institutions:

Wut Mean?

- Banks have been replacing deposit outflows with the borrowing we have covered above.

- ‘Strong and resilient’ indeed….

- It is starting to smell idiosyncratic all up in here:

https://www.marketwatch.com/story/u-s-bank-lending-falls-in-latest-week-fed-says-b633e731

{kind=link}

To me, this is looking more and more like over-reliance on Central Bank Funding!

Oh yeah, The Fed announces the individual capital requirements for all large banks, effective on October 1. The minimum capital requirement is 4.5 percent; The stress capital buffer requirement is at least 2.5 percent.

Betchya those BTFP numbers jump even more!

{kind=link}

Interestingly, the other day the FDIC observed some institutions incorrectly reduced the amount reported to the extent the uninsured deposits are collateralized by pledged assets; this is incorrect as the existence of collateral has no bearing on the portion of a deposit that is covered by federal deposit insurance!:

Wut mean?:

- The FDIC noticed that some banks aren’t correctly reporting the amount of deposits they have that aren’t covered by federal insurance. Some banks mistakenly think that if a deposit is backed by assets (like collateral), it doesn’t need to be reported as uninsured.

- This isn’t right! The deposit’s status doesn’t change just because it has collateral.

- Also, some banks were leaving out deposits made by their own subsidiary companies.

Then on Friday, Heartland Tri-State Bank of Elkhart, Kansas, was closed today by the Kansas Office of the State Bank Commissioner, which appointed the Federal Deposit Insurance Corporation (FDIC) as receiver.

- with $139m in liabilities and $130m in assets

- Usually you would see bank failures happen when the ratios are way out of wack and they go up-side-down quickly because of the massive liability:asset ratio and paired with lots of leverage.

- However, this was not the case, and yet the DIF still needed to step in and cover over 40% of deposits.

- Speculation: Are they caught up in all of this?

TLDRS:

- About half of U.S. banks (2,315) with $11 trillion of assets have a lower value of their assets compared to the face value of their debt liabilities.

- The market value of their assets is about $2.2 trillion lower than the book-value accounting for loan portfolios held to maturity.

- The BTFP buys another day, but will banks be able to survive October’s reserve requirements?

- The FDIC noticed that some banks aren’t correctly reporting the amount of deposits they have that aren’t covered by federal insurance. Some banks mistakenly think that if a deposit is backed by assets (like collateral), it doesn’t need to be reported as uninsured.

- Heartland fails shortly after this notice–connected?

- Reminder, while banks have the liquidity fairy, ‘we’ get the promise of 2 more rate hikes this year, Atlanta Fed President Raphael Bostic yet again enrichens himself inappropriately from his position.

- To fix one end of their mandate (price stability) from the inflation problem they created, the Fed will continue sacrificing employment (the other end of their mandate) to bolster price stability by continuing to raise interest rates–causing further stress to businesses and households.

- I believe inflation is the match that has been lit that will light the fuse of our rocket.