The housing market appears to be spiraling. Many homeowners, even the affluent ones, seem desperate to sell their properties, some resorting to significant price slashes. For instance, a listing in Houston has seen a substantial -12% price cut, yet it remains unsold. This echoes a broader trend: Wall Street investors are shedding their homes in droves.

There’s an urgency in these moves. The personal saving rate in the US has plummeted to 3.4%, the lowest since the Global Financial Crisis. Even more alarming, it’s the lowest since the Great Depression. This rapid spending coupled with inflation is triggering financial strains. Delinquencies on various loans are rising, including mortgages, auto loans, and credit cards. As the economic pressure builds, many Americans are pushing themselves with increased overtime, leading to widespread burnout.

“A lot of owners took on homes and mortgages and extra vacation homes when lending criteria was easier….I feel like everybody’s in panic mode now. Even wealthy owners are asking if I have anybody for their house.”

Maybe last year's 20 print on the NAHB's homebuyer foot traffic was the low. Maybe. But it is back down to 26 again and ugggh, the next report is Thursday. Fed Funds history says watch out. I am mentally preparing for buyer volumes to continue folding like a cheap suit. pic.twitter.com/5hmafmLTvD

2020 BIDEN VOTER: "Well, I didn't see something, like, really change … I'm working three jobs because I have to pay more, like my house is more expensive…" pic.twitter.com/SobJVdwJl1

Boomers doing their 76th cash-out refinance since 1983 expecting a young family to spend 55% of their gross income servicing a mortgage pic.twitter.com/LIL2xQ9aIP

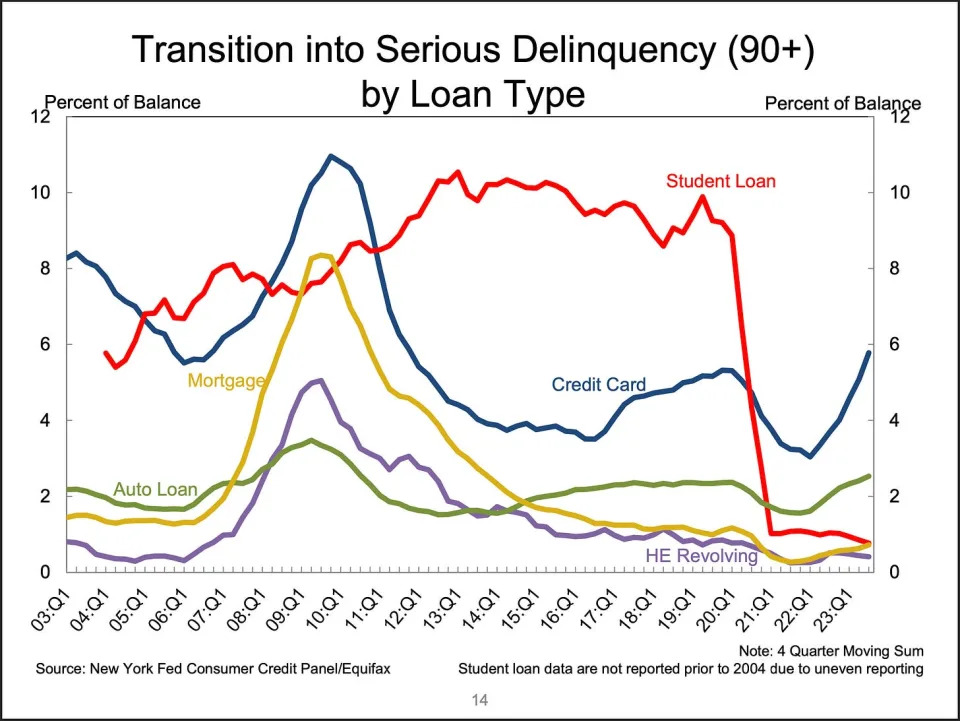

According to the New York Fed’s Q3 Household Debt and Credit (HHDC) report, the share of debt newly transitioninginto delinquency continues to rise for mortgages, auto loans, and credit cards.

When you include the debt, the delinquency rates, while rising, continue to reflect a normalization back to prepandemic levels.

Americans now owe $1.08 trillion on their credit cards, the Federal Reserve Bank of New York reported Tuesday.

Balances jumped 15% from a year ago, according to a separate quarterly credit industry insights report from TransUnion, while the average balance per consumer hit $6,088, the highest in 10 years.

Trained professional helps woman deal with grocery inflation:

This is funny but true, and it happened to me the other day while shopping with my wife.

Americans are working increasing overtime hours to make up for worker shortages, leaving them burnt out.

"Why is daddy not home to take me out trick-or-treating … Try to explain mandatory overtime to an eight-year-old,” a Boston EMT says. https://t.co/WC1PwDUOJy