by Chris Black

Despite the Federal Reserve’s “stealth easing (https://www.concoda.com/p/the-stealth-liquidity-squeeze)”, dollar strength has begun to accelerate once again.

Usually, this is not the case, as dollars will deploy into either risk assets or safe assets depending on the environment.

But as liquidity subsequently drains, the world’s response will not be to de-dollarize but to seek more dollar liquidity. The U.S. central bank’s global swap network is set to expand.

Back in 2019, before the Fed unleashed trillions of dollars in liquidity to stem COVID fears, global markets had entered a lengthy “excess collateral” era.

The Fed’s RRP (reverse repo) facility, a shock absorber for excess cash and the de-facto measure of surplus liquidity, lay empty.

Almost every dollar was being deployed by private sector entities into trades that did not alter the Fed’s balance sheet, from repos (https://www.concoda.com/p/the-treasury-market-unwind) funding leveraged Treasury investors to Eurodollar arbitrage by New York branches of foreign banks.

Soon, however, a relatively unknown trade was not only about to upend the excess collateral era but also the illusion of financial stability in the Fed’s post-crisis (https://www.concoda.com/p/the-federal-reserve-endgame-is-not) system.

Midway through September 2019 on the 17th, a funding squeeze caused (https://www.newyorkfed.org/medialibrary/media/research/epr/2021/EPR_2021_market-events_afonso.pdf) money market rates to skyrocket.

The Fed’s SOFR (https://www.newyorkfed.org/markets/reference-rates/sofr) (Secured Overnight Financing Rate), a measure of the average cost to borrow cash secured against U.S. Treasuries, showed repo rates spiking above a whopping 5%.

Meanwhile, in a frantic search for other sources of dollar funding, financial entities had even begun tapping the once-lifeless interbank funding market (https://www.concoda.com/p/the-death-of-the-interbank-market), sending the Fed Funds rate (EFFR (https://www.newyorkfed.org/markets/reference-rates/effr)) above the U.S. central bank’s upper limit of its target range.

The Fed responded with a Standing Repo Facility (https://www.newyorkfed.org/markets/repo-agreement-ops-faq), and the “repocalypse” subsided. But the Fed’s bottomless interventions were no longer the major astonishment.

The system was not as stable as monetary leaders and prominent financial players had assumed. It was soon revealed that most market players knew on the day of the repocalypse that liquidity was about to grow scarcer than usual.

Days before, most were aware that corporations would be pulling large sums of cash from MMFs (money market funds) to fund quarterly tax payments, while the U.S. Treasury would be issuing additional government securities into an increasingly illiquid market. Both would pull liquidity — in the form of reserves — from the banking system into the TGA (https://www.fiscal.treasury.gov/tga/), the government’s bank account housed inside the Federal Reserve System.

At the same time, those same financial actors had been assigning large quantities of reserves to trades in the repo market.

While dealers increased their repo borrowing to a point where their inventories — and thus their balance sheets — had reached near capacity, lending in repo became (https://substackcdn.com/image/fetch/w_1456,c_limit,f_webp,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fa3e202af-7c21-40c7-81aa-5f26138c91f4_2601x1824.png) so profitable that banks made more deploying reserves into repos than depositing these at the Fed and earning IOER (https://www.federalreserve.gov/monetarypolicy/reserve-balances.htm) (interest on excess reserves).

{kind=link}

These decisions were also made in the depths of the Fed’s first official QT (quantitative tightening) program, which aimed to drain billions in reserves from the financial system every month.

All in all, the late-2019 repo market had become a ticking timebomb.

Yet in the aftermath and throughout the repocalypse, another funding market undergoing mild stress had barely been covered in the media: the $4 trillion-a-day FX swap market.

As smaller participants failed to locate funding both in repo and the interbank markets, the rate to borrow dollars secured against foreign currencies spiked, though only slightly.

But it was merely a few months after the repo spike faded from mainstream circles that we’d not only discover what real stress in the FX swap market looked like. The world would also come to acknowledge the Fed’s global dollar swap network as the FX swap market’s sole rescue mechanism in times of crisis. The COVID-19 financial panic had emerged, and with it emerged swap lines.

As pandemic fears spread, every one of the 25+ major dollar funding markets (https://telegra.ph/file/050afad4b39424fcf0650.png) began to seize up, including the four-trillion-dollar-a-day FX swap goliath.

{kind=link}

Market participants worldwide, looking to source dollars for currency hedging and liquidity needs, suddenly had to pay a premium to enter into FX swap contracts, the near equivalent of “currency repos”.

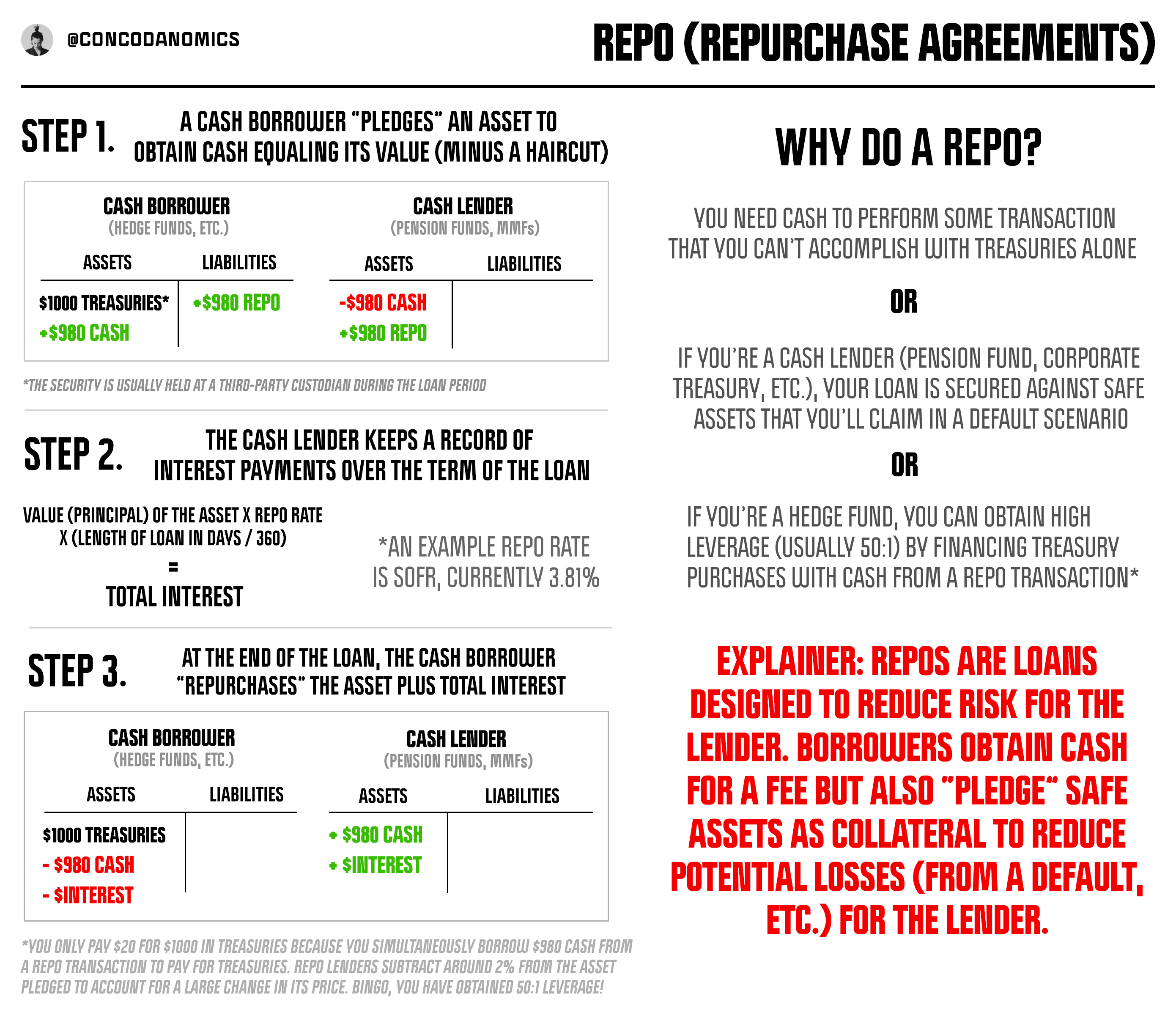

In a currency repo (short for repurchase agreement (https://substackcdn.com/image/fetch/f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fdf6f675f-fe9c-482e-85ae-1783a892bbc5_2781x2388.png)), two parties swap currencies at the present (spot) exchange rate while agreeing at a later date to reverse the swap at the present forward rate.

{kind=link}

This allows participants to lock in today’s exchange rates for a fee, protecting themselves from adverse (but also favorable) currency moves. While standard repos are classed as on-balance sheet assets and liabilities, currency repos are recorded off-balance sheet — as payments can only occur at the maturity of the swap contract.

During the COVID panic, dollars became so scarce via the usual venues of repo and Eurodollar markets that dealers called upon currency repos (FX swaps) to secure liquidity. But they soon discovered that even in FX swaps, dollars had grown scarce.

Their usual FX dealers were unable to provide the goods. They had to go elsewhere.

First, they turned to the New York branches of foreign banks, “the private dealers of first resort”. In non-crisis periods when markets grew imbalanced, foreign banks subject to lax regulation and with greater access to dollar funding stepped in to make markets in FX swaps.

Still, despite these trades now yielding greater profits via wider bid-ask spreads, foreign banks pulled back, not wanting to expose themselves to market volatility that would breach internal protocols.

The next avenue for dollar liquidity seekers was to tap the Wall Street megabanks: the private dealers of last resort. Yet, they got the same response.

Despite spreads widening enough to attract large U.S. banks repressed by Basel III regulations (https://www.bis.org/bcbs/basel3.htm), the Wall Street goliaths also pulled back from FX swap market making. Internal risk limits and regulatory constraints (https://substackcdn.com/image/fetch/f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fa45fc144-56b1-465b-a9db-3630f405c80d_864x385.jpeg) meant that even JPMorgan and its “Bakken Shale (https://plus2.credit-suisse.com/content/getsourcedocument?Document_ID=1b4CAV&format=pdf)” of reserves were no match for COVID-19’s volatile conditions.

{kind=link}

Now that the ultimate private dealer of last resort was hindered, the public dealer of last resort was primed and ready to step in.

The Federal Reserve’s dollar swap lines were about to be activated. On March 15, 2020, FX swap markets broke down completely.

In no time at all, the Federal Reserve along with other G7 central banks announced the resurgence (https://www.bankofengland.co.uk/news/2020/march/coordinated-central-bank-action-to-enhance-the-provision-of-global-us-dollar-liquidity) of U.S. dollar swap lines.

By offering to provide unlimited liquidity at its “upper global jaw (https://x.com/not_concoda/status/1709648394434605157),” which cost OIS (the overnight indexed swap rate) plus 0.25%, the Fed caused volatility to subside.

The private dealers of first and last resort returned, bringing the FX swaps market back into balance. Prominent FX swap dealers in G7 countries, from Japan to Canada, cried out to their regional central banks for dollar liquidity, who in turn called up the Fed, creating an intricate web of dollar loans and claims.

The FX swap bailout was complete.

At the time, the dollar had already secured its spot as the dominant global currency (https://www.bis.org/publ/cgfs65.pdf), making up half of all trade invoices, cross-border loans, and international debt securities. 88% of all FX trades involved the dollar, while ~59% of all foreign exchange reserves were dollar-denominated.

The FX swap lines and their effectiveness during COVID simply added an extra dimension to the world’s dollar dependency, along with that of the other 25 comprehensive funding markets — like repo and Eurodollars , none of which have run into compelling rivals.

The vast majority of countries and nations are no longer using the global dollar system: they are part of it, acting as connectors to bridge trillion-dollar imbalances in global markets daily, without central banks and governments ever intervening.

But when no one else comes to the rescue, the only backup monetary leaders have developed is the Fed’s dollar swap network.

What’s more, they are becoming more – not less – attached to it, deploying liquidity lines swifter than ever before.

In the March collapse of Silicon Valley Bank (https://t.me/DissidentThoughts/2335) and the bailout (or bail-in ) of Credit Suisse, swap lines were activated at the first sign of hazard.

So when another monetary emergency strikes, the same swift response is assured.

The golden age of the Federal Reserve acting as “the swapper of last resort” looks to have only just begun, and with each intervention that global leaders submit to, de-dollarization only becomes an increasingly distant fantasy.